「貯金は裏切らない?|お金を働かせる時代へ:増やす力の極意」

今日は【増やす力】

投資を始めて資本家になろう

というお話をします。

お金の大事な流れというのは

「貯める力」

↓

「稼ぐ力」

↓

「増やす力」

↓

「守る力」

↓

「使う力」

です。

この5つの力を育んでいこうという中で

誰にでも大事なところ。

一番最初にやって効果が出やすいので

『貯める力』を今までお話ししてきました。

今後は『増やす力』編に入りたいと思います。

●目指す所

大体

お金の無い人=お金に困っている人というのは

どういう流れになっているのか。

(生活苦の仕組み 出典:リベラルアーツ大学)

収入の柱が一本しか無くて

税金をここでジャブジャブ取られる。

なんとか少しの資産を貯めようとしてるんけど

そこで貯まったものを浪費に流して

投資には流さない。

こうなるとやはり生活が苦しくなる。

何が浪費に当たるのか?

という事を今までお話ししてきました。

●浪費をせき止め投資にまわす

(税金徴収の仕組み 出典:リベラルアーツ大学)

ここをまず目指したい。

収入の柱は一本だが

浪費をせき止めて

消費から投資に流していきたい。

一番理想的なお金の流れというのは

(理想的なお金の流れ 出典:リベラルアーツ大学)

収入の柱=水の流れが複数あって

浪費には流さず

投資にドンドン流す。

投資に流すと

またこれが新たな収入源になって

水を流してくれる。

この状態を目指したい。

浪費をせき止めるという作業は

今までのお話でご理解頂けたと思います。

今後投資に流していくという所ですね。

この部分を勉強していきたい。

投資というのが

わかるようなわからないような

曖昧な状態ではないかと思うので

イチからやっていきたいと思っています。

●投資について

日本人で投資をしている人は

大体20〜30%程度と言われています。

投資とはお金に働いてもらう事です。

資本家側になる第一歩と言うことですね。

・株

・不動産

その他色々あります。

●何故投資をする必要があるのか

前にもお話しした事がありますが

所得が上がっていく=増えていくスピード

給料が増えていくスピードよりも

支出が増えていくスピードの方が速い。

(出典:Wikipedia)

フランスの経済学者トマ・ピケティが言った式が

r(リターン)>g(グロース経済成長)

これは投資をしないと

ドンドン貧乏になる世の中である

ことを示しています。

簡単に言うと

「だから投資をしよう!」

という事ですね。

労働だけでお金持ちになるのはやはり難しい。

・給料が上がりづらい。

・貯まるスピードも遅い。

なぜかと言うと

貰った給料からもろもろ自動で搾取される。

毎年勝手にたくさん搾取されてしまう。

もしくは

年々自分のパフォーマンスが下がっていく。

年を取れば取るほど

基本的にはパフォーマンスは下がる。

経験でカバー出来る所が有ったりするが

年功序列制度というのはもう崩壊してます。

いつ何が有っても

大企業であってもどうなるかわからない。

自分が働けなくなったら終わってしまう。

なので投資に回して収入の柱を増やしたい。

●なぜ投資をする必要があるのか

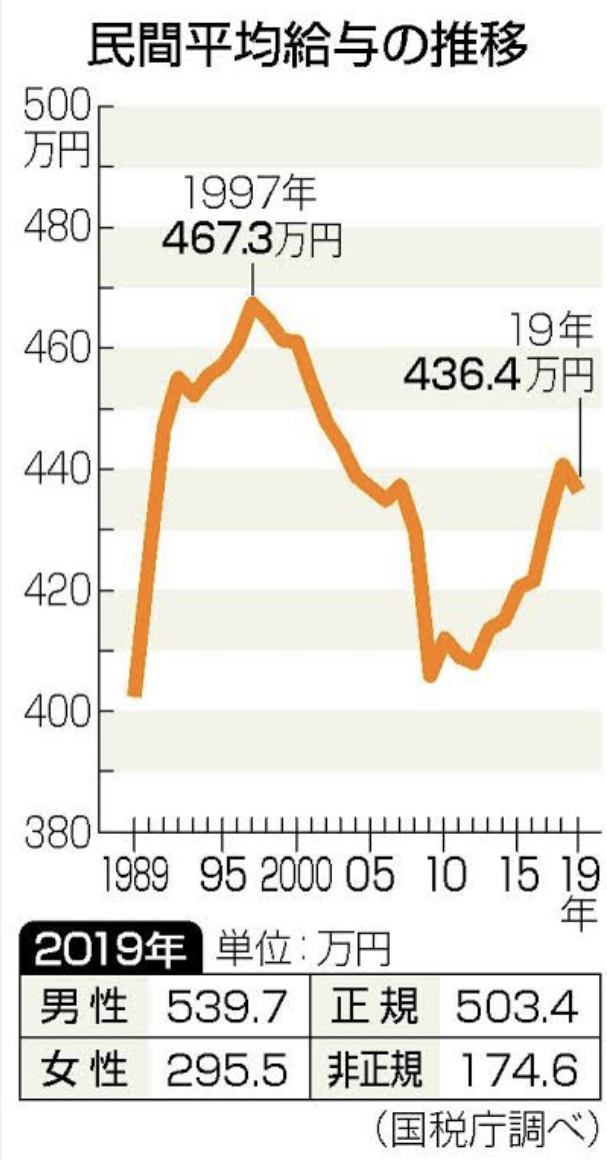

給料が25年前から変わっていない。

日本の給料、民間平均給与の推移は

平均の給料というのが

バブルの時をピークに落ちてます。

結局2009年まで

全然上がってきてない。

その割に

サラリーマンの方であれば

ほぼ入っているであろう社会保険料。

これが増え続けている。

(出典 日本経済新聞)

社会保険=健康保険と厚生年金ですが

上がり続けてきています。

負担が増えている。

年収700万円の人で

この10年間で

年間の社会保険料の負担は

20万円も増加しています。

要は負担が増えている。

毎月天引きされている

金額が増えています。

収入が伸び悩んでいるのに

支出だけ右肩上がりを続けている。

●減る年金

これはよく話題になってますけど

年金もほぼ確実に減ります。

色々議論されているので

細かいことはもう言わないです。

年金というのがほぼ確実に減ります。

将来貰える年金はほぼ減る。

●インフレの恐怖

「では貯金をしておこう!」

という発想になると思います。

貯金をしておいたら

とりあえず減らないと思ってませんか?

貯金は裏切らないのか!?

では過去のデータから見ていきましょう。

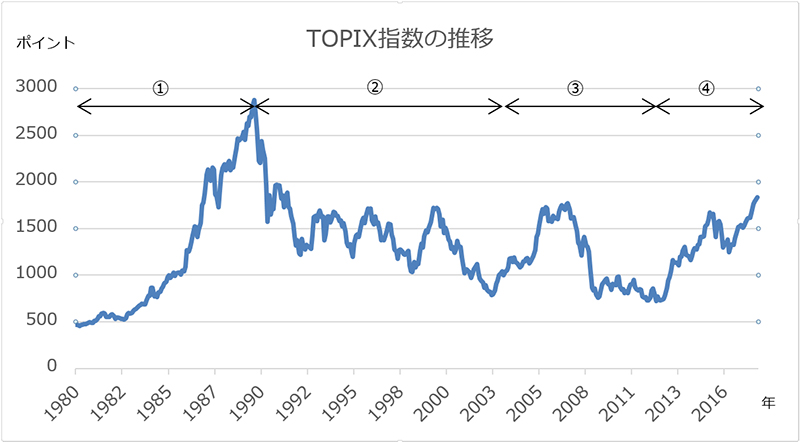

1990〜2000年前半の日本というのは

土地の価格がずっと下がりつづけていました。

株価(TOPIX)=日本の平均株価を見ると

1990年以降これもずっと下がりつづけてきた。

確かに土地や株を一番高い時に買った人というのは

ずっと苦しい時期がつづいていた。

なかなか厳しい時代だったんですよね。

確かにこの時は

貯金が最強の時期だったんです。

日本円を貯める事においては

現金で持っておくというのが

確かに一番正しい選択でした。

一番ピークの所で

土地や株を買った人たちは

1/3〜1/4ぐらいになっている。

結構厳しい状態ですよね?

~~~つづく~~~

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約≫≫

要約: 「増やす力」を育てる重要性

●お金の流れ

お金の流れは、「貯める力」→「稼ぐ力」→「増やす力」→「守る力」→「使う力」の順で成り立ちます。これら5つの力をバランスよく育てることが重要です。

●今までの話: 貯める力

これまで「貯める力」の重要性について話してきました。節約して浪費を防ぐことが第一歩です。

●今後の話: 増やす力

これからは「増やす力」について学んでいきます。増やす力とは、投資を通じてお金を働かせる力のことです。

●投資の必要性

1.収入の柱を増やす: 収入の柱が一つだけではリスクが高い。浪費を抑え、投資に回すことで収入源を増やすことが目標。

2.投資の少なさ: 日本では投資をしている人は20〜30%程度。資本家になるためには投資が必要。

3.経済の現実: 給料の増加スピードよりも支出の増加スピードが速い。フランスの経済学者トマ・ピケティの式「r(リターン)>g(グロース経済成長)」が示す通り、投資をしないと貧しくなる可能性が高い。

●給料と支出の現実

日本の平均給与はバブル期をピークに落ち続けていますが、社会保険料の負担は増え続けています。年収700万円の人でも、この10年で年間の社会保険料が20万円増加しました。

●将来の不安

年金はほぼ確実に減り、インフレも恐怖です。貯金だけではお金が減るリスクがあります。

●過去の教訓

1990〜2000年前半の日本では、土地と株価が下がり続けました。現金を持っておくのが最も安全な選択でしたが、今後も同様であるとは限りません。

これからの講義では、投資について具体的に学び、どのようにして「増やす力」を身につけるかを探っていきます。

≪≪Chat-GPTくんによる英訳≫≫

【Today’s Topic: The Power to Increase】

Let’s talk about starting investments and becoming a capitalist.

【The Important Flow of Money】

The important flow of money follows this sequence:

1.The Power to Save

2.The Power to Earn

3.The Power to Increase

4.The Power to Protect

5.The Power to Spend

These five powers are crucial for everyone to cultivate. We have previously discussed ‘The Power to Save’ as it is the first step that shows results quickly.

【Moving Forward: The Power to Increase】

We will now move on to the ‘Power to Increase’ series.

【The Goal】

Typically, people who have no money and are struggling financially experience the following pattern:

・They have only one source of income and are heavily taxed.

・They try to save a little but end up wasting what they save instead of investing it.

This leads to financial hardship. We have previously discussed what constitutes wasteful spending.

【Stop Wasteful Spending and Direct Funds to Investment】

Our initial goal is to stop wasteful spending and direct funds from consumption to investment.

The ideal flow of money is to have multiple sources of income and direct funds toward investment instead of wasteful spending. Investments then become new sources of income, creating a continuous flow of funds.

Stopping wasteful spending has been covered in our previous discussions. Now, we will focus on directing funds to investment.

【Learning About Investment】

Investment might seem ambiguous, so we will start from the basics.

【About Investment】

In Japan, only about 20-30% of people invest. Investment means making your money work for you. It is the first step to becoming a capitalist. Investment options include:

・Stocks

・Real Estate

・arious other assets

【Why is Investment Necessary?】

We have previously discussed that the speed at which income increases is slower than the speed at which expenses increase.

French economist Thomas Piketty’s formula, r (return) > g (economic growth), indicates that without investment, people will become poorer over time.

Simply put, this is why we should invest. It’s challenging to become wealthy through labor alone because:

・Salary increases are slow.

・The speed of saving is also slow due to automatic deductions from salaries.

Additionally, as we age, our performance tends to decline. The seniority-based system is collapsing, and even large corporations are no longer guaranteed to be stable. If you become unable to work, it’s over. Therefore, increasing the number of income sources through investment is essential.

【The Need for Investment】

Salaries have not changed for 25 years. The average salary in Japan peaked during the bubble economy and has not significantly increased since 2009. Meanwhile, social insurance premiums continue to rise.

For someone with an annual income of 7 million yen, social insurance premiums have increased by 200,000 yen in the past 10 years, indicating an increasing financial burden despite stagnant income.

【Decreasing Pensions】

Pensions are almost certain to decrease in the future. There is no need to delve into details as it is widely discussed. The amount of pension one can expect to receive will almost certainly decrease.

【The Fear of Inflation】

You might think, “Then let’s save money!” But will saving money ensure it doesn’t decrease?

Looking at past data:

・From 1990 to the early 2000s, land prices in Japan continuously decreased.

・The average stock price (TOPIX) also declined steadily from 1990 onwards.

During this period, holding cash was indeed the best choice as those who bought land or stocks at their peak saw their value drop to one-third or one-fourth. It was a tough time, and holding cash was the safest bet.

However, the situation may not always be the same moving forward.

Special Thanks OpenAI.