「お金の舞台裏|税金と社会保険解剖してみた」

今日は【守る力】

今までのお話のまとめを

お話します。

●知識が武器~税金のルールをあなたの味方に~

税金の事は

学校では教えてくれません。

まずは知る事が大事です。

知る事は

盾にもなり武器にもなります。

賢い人達が作ったルールを

上手く使っていく。

やはり

「税金高い!」

「知らなかった」

と文句を言ってても

しょうがないんです。

どの国でもそうですけど

やはり賢い人たちが

自分達に有利なように出来てるというのが

この国のルールなので

文句を言ってても仕方がないので

このルールを上手く使う方になる

というのが大事です。

●税金は敵じゃない~仕組みを理解し味方にしよう~

税金についてですが

主に給料や所得に対してかかるのは

所得税と住民税です。

(1)所得税

5〜45%です。

会社員は先払いしています。

毎月天引きしている。

それが『源泉徴収』です。

事業主の場合は

翌年の3月にまとめて払います。

(2)住民税

どこに住んでても一律10%です。

会社員はこの住民税を

後払いしてるんです。

去年の分の住民税を

今年払っていってる。

その天引きのことを

『特別徴収』と言います。

事業主は翌年の6月から

一括だったり分割だったりで

払っていきます。

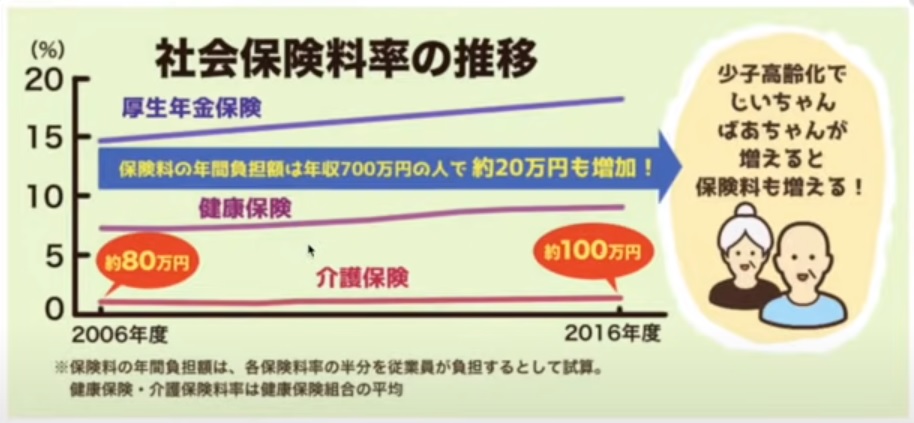

●社会保険料の負担~年々上がるその現実を見逃すな~

社会保険はこれも言うなれば税金です。

これが本当に手取りを減らす

大きな原因です。

本当に毎月天引きされてるこの社会保険

負担がすごく大きいんですよ。

(社会保険料率の推移 出典:リベラルアーツ大学)

この社会保険料率の推移は毎年ずっと

コツコツ上がりつづけてるんですよ。

すごく高くなっていて

10年間で20万円も負担が増加しています。

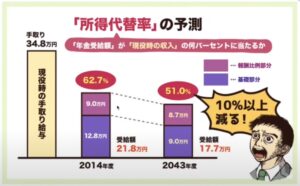

●年金は減る一方、支払いは増える~賢くコントロールしよう~

もらえる年金も

ほぼ確実に減ります。

(所得代替率の予測 出典:リベラルアーツ大学)

支払いの負担は増えていってるのに

もらえる年金はほぼ確実に減るんですよ。

だから

・うまく

・合法的に

コントロールしていかないといけない。

●社会保険の仕組みを知ることが、未来の安心につながる

社会保険には以下のものがあります。

・医療保険

・年金保険

・労働保険

これだけ色んな種類があり

国民健康保険と国民年金は

事業主が入る保険です。

会社員は

・健康保険

・厚生年金

・雇用保険

・労災保険

に入る。

会社員は会社が各項目

半分負担してくれています。

●支払いタイミング、会社員と事業主で違う~自分に合った対策を~

支払いの時期ですが

(1)会社員の場合

毎月給与から天引き

(2)事業主の場合

年に一回もしくは分割

課税所得に応じてかかってきます。

●節税の基本は課税所得の管理~会社員も事業主も賢く対策~

税金の計算方法ですが

税金は課税所得にかかる。

この課税所得を減らすという事が

節税になっていくという事です。

会社員の場合は

給与ー控除=課税所得

事業主の場合は

売上ー経費ー控除=課税所得

この課税所得に対して税金はかかる。

社会保険は給与にかかるんですよね。

額面にかかるんですよ。

4〜6月の平均報酬月額に対してかかります。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

税金のルールを理解し、賢く活用することが大切です。学校では教えられないことが多く、知ることが最初のステップです。知識は盾にも武器にもなります。主な税金は所得税(5〜45%)と住民税(一律10%)で、会社員は源泉徴収で先払いしています。一方、事業主は翌年の3月にまとめて支払います。住民税も会社員は後払いで、去年の分を今年払います。

社会保険料は実際に手取りを減らす大きな原因です。この料率は毎年上昇しており、10年間で約20万円の負担増加しています。さらに、年金受給額は減少傾向にあります。

社会保険には医療保険、年金保険、労働保険があります。会社員と事業主で加入する保険が異なり、会社員は健康保険、厚生年金、雇用保険、労災保険に加入します。会社は各項目を半分負担しています。

支払いの時期も異なります。会社員は毎月給与から天引きされ、事業主は年に一回または分割で支払います。

税金の計算方法は、課税所得に基づきます。会社員の場合、給与から控除を引いた額が課税所得となり、事業主の場合、売上から経費と控除を引いた額が課税所得です。社会保険料も給与(額面)に対して計算されます。この知識を活用することで、税金と社会保険の仕組みを賢くコントロールし、未来の安心につながります。特に、課税所得を減らすことが節税の基本であり、会社員も事業主も賢く対策を立てることが重要です。

Citations:

[1] https://www.yayoi-kk.co.jp/shinkoku/oyakudachi/juminzei/

[2] https://www.mmea.biz/simulation/calculation/

[3] https://www.pref.iwate.jp/kensei/zei/gaiyou/chuugaku/1011224.html

[4] https://www.ht-tax.or.jp/kigyou-guide/tax-saving-measures-2

[5] https://www.nta.go.jp/taxes/kids/hatten/page14.htm

[6] https://www.city.shibata.lg.jp/kurashi/zei/zeikin/shiminzei/faq/1000679.html

[7] https://biz.moneyforward.com/payroll/basic/56616/

[8] https://www.shiruporuto.jp/public/document/container/shotokuzei_shikumi/

[9] https://www.saisoncard.co.jp/credictionary/knowledge/article100.html

[10] https://www.moj.go.jp/isa/content/930004446.pdf

[11] https://www.rakuten-card.co.jp/minna-money/tax_deductible/article_2012_00002/

≪≪Chat-GPTくんによる英訳≫≫

Today’s Topic: The Power to Protect

I will summarize everything we’ve discussed so far.

—

【Knowledge is Power – Make Tax Rules Your Ally】

Taxes are not something schools teach you about.

The first thing is to understand them.

Knowing is both a shield and a weapon.

We need to learn how to make the rules created by the smart people work in our favor.

It’s no use complaining about:

– “Taxes are high!”

– “I didn’t know!”

Complaining won’t help.

This is true in any country. The rules are made by the smart people who set them up to benefit themselves.

So, complaining is not going to change anything. The key is to learn how to use these rules to your advantage.

—

【Taxes Are Not the Enemy – Understand the System and Make It Your Ally】

When it comes to taxes, the main ones that apply to income and salaries are:

– Income Tax

– Resident Tax

1. Income Tax

It ranges from 5% to 45%. Employees pay it in advance through payroll deductions, called “Withholding Tax.”

For business owners, it is paid all at once in March of the following year.

2. Resident Tax

It is a flat 10% regardless of where you live.

For employees, this tax is paid in arrears, meaning they pay for the previous year’s tax in the current year. This is called “Special Collection.”

For business owners, the tax is paid in full or in installments starting in June of the following year.

—

【The Burden of Social Insurance – Don’t Miss the Reality of Its Yearly Increase】

Social insurance can be considered another form of tax.

This is one of the biggest reasons your take-home pay decreases.

Social insurance is deducted from your salary every month, and the burden is significant.

(Reference: Social Insurance Rate Changes, Liberal Arts University)

The rate for social insurance has been steadily increasing year by year. It has become very high, with a 200,000 yen increase in the past 10 years.

—

【Pensions Are Decreasing While Payments Are Increasing – Control It Wisely】

The amount of pension you can receive will almost certainly decrease.

(Reference: Predicted Income Replacement Rate, Liberal Arts University)

While the burden of payments is increasing, the pension you will receive is almost certainly decreasing.

Therefore, you need to:

– Control it wisely

– Do so legally

—

【Understanding the Structure of Social Insurance Leads to Future Security】

Social insurance includes the following:

– Health Insurance

– Pension Insurance

– Employment Insurance

There are many types, and both National Health Insurance and National Pension are insurances for business owners.

For employees, they are enrolled in:

– Health Insurance

– Welfare Pension

– Employment Insurance

– Workers’ Compensation Insurance

The employer covers half of the contributions for each of these categories.

—

【Payment Timing Varies for Employees and Business Owners – Plan Smartly for Your Situation】

As for the payment timing:

1. For Employees:

It is deducted from their monthly salary.

2. For Business Owners:

It is paid either once a year or in installments.

The payment amount is based on taxable income.

—

【The Key to Tax Savings is Managing Taxable Income – Smart Planning for Employees and Business Owners】

Regarding how taxes are calculated:

Taxes apply to taxable income.

Reducing taxable income is the key to tax savings.

For employees:

Salary – Deductions = Taxable Income

For business owners:

Revenue – Expenses – Deductions = Taxable Income

Taxes are applied to this taxable income.

Social insurance applies to your salary. It is based on the gross amount.

It is calculated based on the average monthly salary from April to June.

—

Special Thanks OpenAI and Perplexity AI, Inc