「被害に備える新たな視点|地震保険の本質教えます」

今日は【貯める力】

地震保険は必要か?

というお話しします。

●地震保険の真実!知らなかった補償と加入のポイント

地震保険とは

地震・噴火・津波による

火災や埋没

すなわち火災による損害を

保証してくれる保険です。

要は

地震とか噴火とか津波による損害を

保証してくれる。

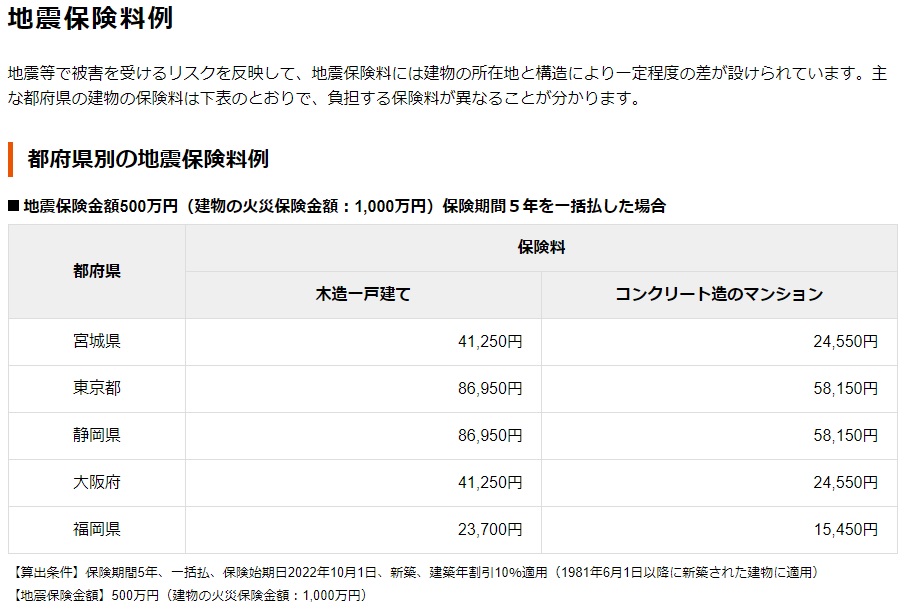

世帯加入率は

全体の3割弱の人が入ってます。

住む場所によって

保険料が違います。

(出典:https://www.sonysonpo.co.jp/fire/fp018.html)

地域やその年によって

違うんですけど

東京と福岡では

3.67倍違ってきます。

それから

火災保険とセットで

入るんですよね。

地震保険

単体では入れないんですよ。

建物に2千万円の

火災保険をかけた場合

地震保険の上限というのは

1千万円

要は

火災保険の50%分しか

地震保険というのはかけられないです。

火災保険が2千万円かけた場合には

1千万円になる。

地震による火災は

地震保険でないと保険がおりません。

だから入るという人も結構いる。

どこの保険会社でも

保証内容とか保険料というのは

実は変わらないんですよね。

地震保険というのは

実は政府と損害保険会社というのが

共同で運営していて

保証内容や保険料は一律です。

火災保険の半額までしか入れない

ということも決まってるんですよね。

さらに上限金額があって

建物の場合5千万円まで。

家財の場合1千万円までという

上限金額というのも決まってるんですよ。

最大でかけられる金額

というのも決まっています。

どこの保険会社でも

保証内容や保険料は

一律なんですけど

どうして

色んな保険会社で

値段の違いが出るかというと

火災保険とセットだから

なんですよね。

火災保険部分というのは

各社によって差が出てくるので

結果的に地震保険にも

差が出るんですよね。

だから見比べる必要があります。

●知って安心!地震保険の4段階補償で被害に備える

(出典:https://www.sonysonpo.co.jp/fire/fp014.html)

地震保険における

建物の損害区分は

被害状況により

以前は3段階でしたが

平成29年に4段階になりました。

例:2千万円火災保険をかけてた場合

(1)全損

地震等により損害を受け

損害額が保険の対象である家財全体の

時価額の80%以上となった場合

→1千万円(100%)

(2)大半損

地震等により損害を受け

損害額が保険の対象である家財全体の

時価額の60%以上80%未満となった場合

→600万円(60%)

(3)小半損

地震等により損害を受け

損害額が保険の対象である家財全体の

時価額の30%以上60%未満となった場合

→300万円(30%)

(4)一部損

地震等により損害を受け

損害額が保険の対象である家財全体の時価額の

10%以上30%未満となった場合

→50万円(5%)

●地震保険の本当の役割:家ではなく生活を守る保険

地震保険の目的は

建物の再建が目的じゃないんですよ。

地震保険というとイメージで言うと

地震で壊れちゃった家が

直る感じがすると思いますが

そうではないです。

ここが大事なところで

大前提として

おぼえておいてほしいんですけど

地震保険というのは

建物再建が目的じゃないんですね。

生活再建が目的です。

どういう事かというと

例えば

2千万円保険をかけてたとして

2千万円の家が全損して全部壊れて

基礎や柱や梁も

全部流されて壊れたとして

1千万円保険金が出たとしても

再建築できないですよね?

直すにも全損だから直らないし

もう一度建て直すって不可能ですよね?

じゃあ何のために入るのか?

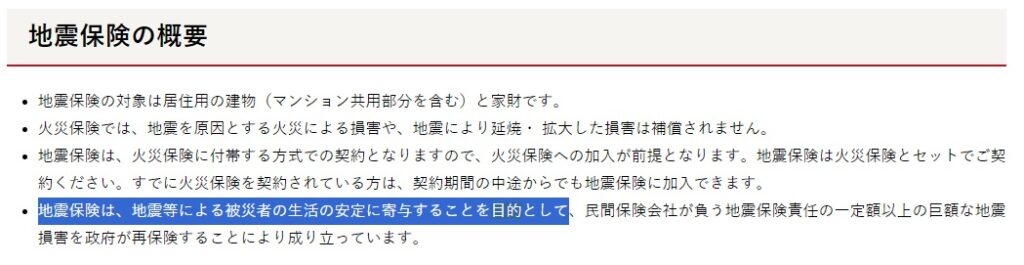

「地震保険は地震等による

被災者の生活の安定に寄与する事を

目的とする」

と財務省のホームページに

書いてあります。

(出典:https://www.mof.go.jp/policy/financial_system/earthquake_insurance/jisin.htm)

だから

そもそも地震保険というのは

どういうものかというと

家を直すものではなくて

生活を再建するための保険

なんですよね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

地震保険は、地震や噴火、津波による火災や損害を補償する保険であり、火災保険とセットで加入する必要があります。日本では世帯加入率は約30%ですが、地域によって保険料が異なり、例えば東京と福岡では最大3.67倍の差があります。地震保険は火災保険の50%までしか加入できず、上限金額は建物5千万円、家財1千万円と定められています。

補償内容は被害状況に応じて4段階に分類され、全損の場合は100%補償、大半損で60%、小半損で30%、一部損で5%となります。しかし、地震保険の目的は建物の再建ではなく、生活の再建にあります。財務省によれば、「地震保険は被災者の生活の安定に寄与すること」を目指しています。このため、地震による火災は通常の火災保険では補償されず、地震保険が必要です。加入を検討する際は、各社の火災保険部分に差があるため、比較検討が重要です。

Citations:

[1] https://www.sonysonpo.co.jp/fire/fp018.html

≪≪Chat-GPTくんによる英訳≫≫

Today’s topic: “The Power to Save – Do You Need Earthquake Insurance?”

【The Truth About Earthquake Insurance: Coverage and Key Points】

Earthquake insurance provides coverage for damages caused by earthquakes, volcanic eruptions, and tsunamis, including fires and burying incidents. In short, it covers losses from natural disasters like earthquakes, eruptions, and tsunamis. Currently, less than 30% of households are enrolled in this insurance.

The premium varies depending on where you live. For instance, there is a 3.67 times difference in premiums between Tokyo and Fukuoka. Earthquake insurance must be purchased as an add-on to fire insurance; it cannot be purchased as a standalone policy.

For example, if you have fire insurance for a building worth 20 million yen, the maximum earthquake insurance coverage is 10 million yen (50% of the fire insurance amount). Fire damage caused by earthquakes is not covered by fire insurance alone, which is why many people choose to purchase earthquake insurance.

All insurance companies offer the same coverage and premiums because earthquake insurance is jointly managed by the government and private insurers. By regulation, you can only insure up to 50% of the value of the fire insurance policy. Additionally, there are caps on the maximum coverage: 50 million yen for buildings and 10 million yen for personal belongings.

Even though the terms of earthquake insurance are standardized across providers, premiums can differ due to variations in fire insurance policies bundled with it. It is important to compare policies carefully.

【Four-Tier Damage Classification for Earthquake Insurance】

As of 2017, earthquake insurance damage classifications have been revised from three tiers to four. For example, if you have fire insurance for a property valued at 20 million yen:

- Total Loss: Damage exceeding 80% of the property’s market value → Payout: 10 million yen (100%).

- Large Partial Loss: Damage between 60% and 80% → Payout: 6 million yen (60%).

- Small Partial Loss: Damage between 30% and 60% → Payout: 3 million yen (30%).

- Partial Loss: Damage between 10% and 30% → Payout: 500,000 yen (5%).

【The True Purpose of Earthquake Insurance: Supporting Your Life, Not Rebuilding Homes】

Contrary to popular belief, earthquake insurance is not designed to rebuild destroyed homes. Its primary purpose is to help individuals rebuild their lives after a disaster.

For instance, even if you receive a 10 million yen payout for a house that was completely destroyed, it would not be sufficient to reconstruct the home. The policy is intended to provide financial support to stabilize your life after such an event.

As stated by the Ministry of Finance, the goal of earthquake insurance is “to contribute to the stability of the lives of disaster victims.” In essence, it is not about repairing or rebuilding a home but about providing a foundation for life recovery.

Special Thanks OpenAI and Perplexity AI, Inc