「木を見て森を見ず|投資?保険?Q&Aで紐解く本当の姿」

〜前回のつづき〜

●Q&A

Q1.保険に入らずに若い時に死んだらどうするんですか?

A.積立保険というのは

そもそも死亡の時に

保険金はほとんど出ません。

出てもわずかというものが

ほとんどです。

それを言うのであれば

若い時に死んだらどうするんだ!!

という事であれば

掛け捨て保険で十分なんですよ。

積立する必要は無いです。

投資信託を買う必要がない。

Q2.積立保険は自分の為ではなく家族に残すものなのでは?

A.それであれば

貯蓄か普通に投資で

いいのではないでしょうか。

わざわざ

割高の投資信託を買う必要は

ありません。

感情論としてはわかりますが

感情で物事を考えちゃうと

話がややこしくなっちゃうので

分けて考えて下さい。

数字で見たら

残すメリットがない。

積立保険に入って

積立で残すメリットが

無いんですよね。

保険は投資のつもりで

入ってないという人もいます。

利回りなんて気にしないし

そんなつもりで入ってないという人も

います。

これは言ってる事が

メチャクチャという所があります。

積立の保険を買うという事は

投資信託を買ってるという事です。

本人の意思とは関係なく

投資信託を買ってる。

だから

投資をしてるという事なんです。

だから

積立の保険を買うという事は

投資信託を買ってるという事です。

しかも割高の。

保険は

なかなかややこしい所もある。

確かにそんなつもりじゃない

というのもわかりますが

実際中身は投資信託なので

そういう認識を持ってもらえればと

思います。

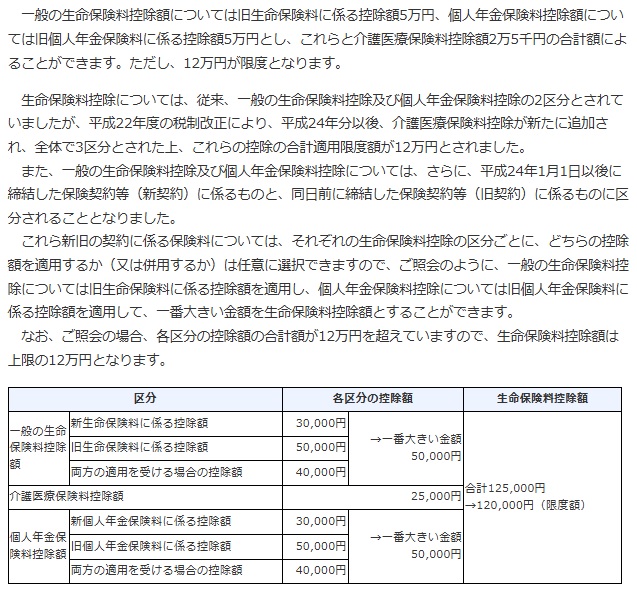

Q3.保険料控除になるからお得なのでは?

A.控除に関しては

節税メリットはあります。

(出典:国税庁HP)

最大で年間12万円なんですよね。

所得税と住民税それぞれ

最大の額が決まってるんですけど

とりあえず控除自体は

最大年間12万円です。

月割りにしたら

1万円程度なんですよね。

毎月1万円ぐらい。

なのにこれ以上かけた所で

控除になりません。

年間12万円以上は

控除にならない。

なのに毎月何万円も

加入している人が結構いたりします。

確かに控除にはなるんですけど

結局割高な手数料を払ってたりとか

保険に関して

色んなお話しをしてきましたけれども

資金拘束だったりとか

短い期間で解約したら

大体元本割れになる。

結局別のリスクも出てくるので

トータルあまりお得ではないと思います。

(出典:https://urerugift.com/column/中小企業の社長が「木を見て森を見ず」だけでは)

木を見て森を見ずみたいになっちゃう。

節税のところだけ見て

入るものじゃないと思います。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

保険に関する議論では、特に積立保険の位置づけが重要です。若い時に死亡した場合の保障を考えると、掛け捨て保険が適切な選択です。積立保険は、家族への資産残しを目的とする場合でも、実際には貯蓄や普通の投資の方が効率的です。積立保険は、実質的に割高な投資信託を購入していることと同じであり、加入者の意図とは無関係に投資をしていることになります。

また、保険料控除のメリットは年間最大12万円(月約10,000円)ですが、それ以上の保険料は控除対象外です。このため、高額な手数料や資金拘束、短期解約時の元本割れリスクを考慮すると、積立保険は必ずしもお得とは言えません。保険選びでは節税だけでなく、総合的な視点での判断が求められます。自身の状況に最適な選択をすることが重要です。

Citations:

[1] https://www.i-hoken.com/column/nenkin-kojo.html

[2] https://www.rakuten-life.co.jp/learn/article/fee/

[3] https://www.tmn-anshin.co.jp/solution/basic/deduction/

[4] https://mponline.sbi-moneyplaza.co.jp/basic/what-deduction-lifeinsurance-2.html

[5] https://www.sonylife.co.jp/examine/knowledge/tax/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Discussion~

【Q&A】

Q1. What happens if you die young without insurance?

A. Savings-based insurance generally pays very little in the event of death.

Even if it pays out, the amount is minimal in most cases.

If your concern is “What if I die young?”

then term life insurance is sufficient.

There’s no need for savings-based insurance.

You don’t need to buy mutual funds through insurance.

—

Q2. Isn’t savings-based insurance for leaving something for your family, not yourself?

A. If that’s the goal, wouldn’t regular savings or investments suffice?

There’s no need to purchase overpriced mutual funds through insurance.

While it’s understandable from an emotional perspective,

mixing emotions into financial decisions complicates matters.

Try to separate the two when making decisions.

From a numerical perspective, there’s no advantage to leaving money through savings-based insurance.

Some people claim they’re not using insurance as an investment or don’t care about the returns.

However, this perspective can be inconsistent.

Buying savings-based insurance is essentially the same as buying mutual funds.

Whether you intend to or not, you are purchasing mutual funds through the policy.

This means you are, in effect, investing.

Moreover, these mutual funds tend to be overpriced.

While it’s understandable that this may not align with your intention,

it’s important to recognize that the contents of savings-based insurance are, in fact, mutual funds.

—

Q3. Isn’t insurance worthwhile because of the tax deductions?

A. Tax deductions do offer some benefits, with a maximum annual deduction of ¥120,000.

The limits for income tax and resident tax are set,

so the maximum deduction remains ¥120,000 annually.

This equates to about ¥10,000 per month.

However, contributions beyond this amount are not deductible.

Despite this, many people pay premiums far exceeding this limit.

While tax deductions are advantageous,

policyholders may end up paying high fees or facing other disadvantages.

For example, funds may be tied up,

and if the policy is canceled within a short period, it often results in a loss of principal.

This introduces additional risks, making the overall benefits questionable.

Focusing solely on tax deductions without considering the bigger picture

is like missing the forest for the trees.

Insurance should not be purchased based purely on the tax benefits.

Special Thanks OpenAI and Perplexity AI, Inc