「高リターン待ってる?保険料の真実に迫る!」

今日は【貯める力】

積立保険で高利回りは可能か?

というお話をします。

●保険のセールストークに騙されるな!~本当に得する選択を~

保険で高利回りは可能か?

結論から言えば

貯蓄性のある保険というのは

全部ゴミ商品です。

ダメ商品ばっかりです。

何故か?

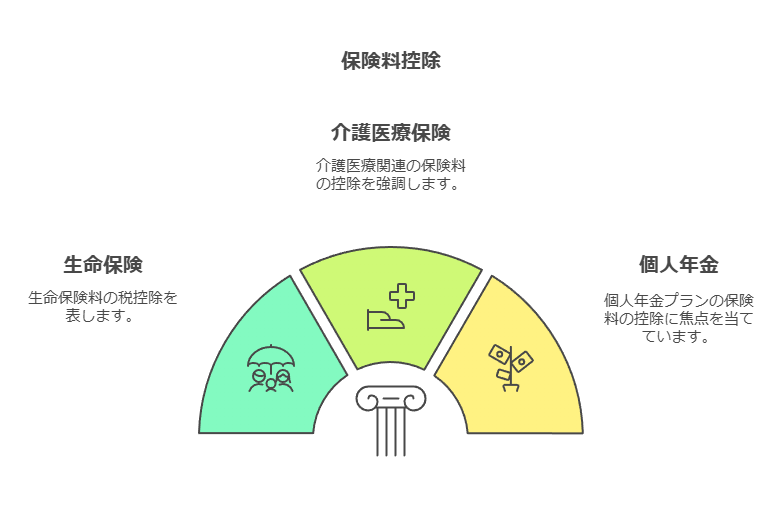

保険料控除についてのおさらいですが

課税所得=売上(収入)-経費-控除

でしたよね?

だから控除を増やすという事が

手取り多いマンになるコツだという

お話しをいままでしてきました。

課税所得を減らすのが

税金を安くする方法ですよね?

サラリーマンの場合は

経費をほとんど使う事が無いので

控除を増やすのが大事なんですよ。

だから

保険料控除を使ったらいいんじゃないか

という事です。

保険料控除にはいくつか種類があって

・一般生命保険料控除

・介護医療保険料控除

・個人年金料保険料控除

とそれぞれ別枠なんですよ。

サラリーマンの場合

保険に入ると

例えば

生命保険に年間8万円

個人年金に同じく8万円

控除される方がいたとします。

控除というのは

しばしばセールストークに使われます。

控除を増やすというのは

確かにお金が戻ってくるので

(払いすぎてる税金が返ってくるだけなんですけど・・・)

控除を沢山増やす事によって

なんだか嬉しい気持ちになります。

なので

心理的なポイントを揺さぶる事によって

「控除になるから保険の方がいいですよ!」

みたいに

結構セールストークに使われるんですよ。

パッと見お得かのように見える。

●保険の利回り幻想に騙されるな~知るべき真実とは?~

なぜダメ商品なのか?

例えば

生命保険に月に9千円かける。

年金保険を月に1万円かける。

保険料控除の節税するメリットと

カード払いで大体1%ぐらいポイントが付く。

カード払いのポイント分を考えると

トータルこの保険に入る事で

利回りが7%になる。

保険会社の営業マンは

こんな主張をしてくるんですよ。

もちろんこの人の所得にもよります。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

積立保険で高利回りを得ることは難しいとされています。保険会社の営業マンが主張する利回りは、保険料控除やクレジットカードのポイントを含めた計算であり、実際の保険商品の利回りとは異なります。

まず、保険料控除には上限があり、税金の軽減効果は思ったほど大きくありません。また、クレジットカードのポイントは一般的に1%程度であり、これを利回りに含めるのは誤解を招きます。さらに、貯蓄性のある保険商品自体は一般的に利回りが低く、他の投資方法と比較して効率が悪いです。

保険会社のセールストークでは、控除や特典を強調し、商品の実質的な価値を誇張する傾向があります。したがって、資産形成を目的とするならば、保険よりも他の金融商品や投資手段を検討する方が賢明です。保険はリスク保障のために利用し、資産形成は別途行うことをお勧めします。

Citations:

[1] https://lify.jp/column/insurance-news/article-73525/

[2] https://www.hokepon.com/prepare/reserve-for-old-age/taxsaving/

[3] https://www.aflac.co.jp/soudan/guide/contents/application/productcreditingrate.html

[4] https://www.tdf-life.co.jp/pre_world5/r_tumitateriritu.html

[5] https://diamond.jp/articles/-/131532

≪≪Chat-GPTくんによる英訳≫≫

Today, I’ll talk about “The Power of Saving” and whether high returns are possible with a savings insurance plan.

【Don’t Be Fooled by Insurance Sales Pitches! – Make the Right Choice】

Can insurance offer high returns?

The conclusion is that all insurance products with savings features are bad investments.

They are all poor products.

Why?

Let’s review the concept of insurance premium deductions.

Taxable income = Revenue (income) – Expenses – Deductions, right?

So, increasing deductions is the key to having a higher take-home income.

Reducing taxable income is the way to lower taxes, correct?

For salaried employees, since they rarely have any expenses to deduct, increasing deductions becomes crucial.

Therefore, using insurance premium deductions could be a good idea.

There are several types of insurance premium deductions, including:

– General life insurance premium deduction

– Medical and nursing care insurance premium deduction

– Private pension insurance premium deduction

These are all separate categories.

For salaried employees, if you join an insurance plan, for example:

– 80,000 yen for life insurance

– 80,000 yen for a private pension

This would reduce your taxable income.

Deductions are often used in sales pitches.

By increasing deductions, you get money back (but it’s just the tax you overpaid being refunded).

This gives people a psychological boost, and many sales pitches play on this feeling.

They often say things like, “It’s better to have insurance because of the deductions,” which may seem like a good deal at first glance.

【Don’t Fall for the Illusion of Insurance Returns – What You Really Need to Know】

Why are these products bad?

For example, if you pay 9,000 yen a month for life insurance and 10,000 yen a month for pension insurance, you’re getting the benefits of insurance premium deductions and about 1% cashback from card payments.

Considering the cashback from card payments, the total return on this insurance plan may seem like it’s 7%.

Insurance salespeople often make such claims.

Of course, this depends on the individual’s income.

Special Thanks OpenAI and Perplexity AI, Inc