「分けて考える|相続税対策に必須!不動産評価のポイント」

〜前回のつづき〜

●不動産の価値、実はひとつじゃない~知って得する『一物五価』の考え方~

不動産の評価方法というのは

・土地

・建物

分けて考えるんですよね。

土地は

・路線価

・固定資産税評価額

に基づいて決めるんですよね。

実際の売買価格ではないと

覚えておいて下さい。

建物も同じで

固定資産税評価額に基づいて決める。

実際の売買価格ではないんですよ。

5000万円で買った家だから

5000万円の財産になる

という訳ではないんですね。

なぜ土地と建物を分けて

計算するのかという事なんですけど

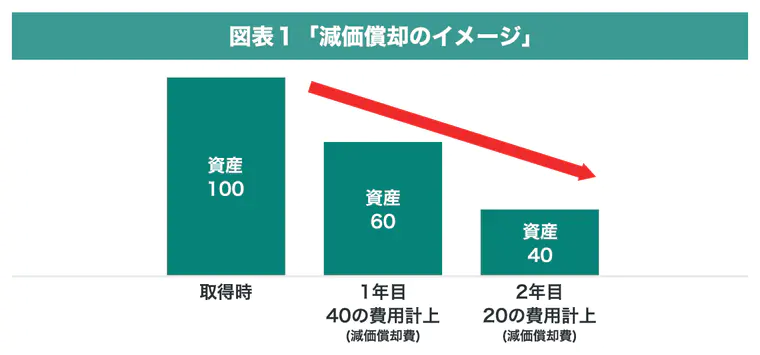

建物は損耗するけど土地は損耗しない。

土地は30年使っても

別にすり減ったりはしない。

土地としては損耗してないですよね?

でも建物というのは30年使ったら

ある程度やっぱりボロボロになる。

損耗していきますよね?

(出典:https://www.nihon-ma.co.jp/columns/2022/x20220323_01/)

減価償却があるかどうかも

一つのポイントです。

要は

建物がグレードアップした場合とか

色々あるので

土地と建物というのを

ちゃんと分けて考えておかないと

正確に計算できないという事です。

『一物五価』って覚えてますか?

過去に

不動産投資のお話しをしたんですけど

不動産はモノとしては一個なんだけど

5つの価格があるんですよね。

・公示価格

・基準値標準価格

・路線価

・固定資産税評価額

・実勢価格

の5つがあります。

実勢価格というのが

一般に売買されてる金額ですよね?

実勢価格が一番高い事が多いんですよ。

相続税を計算するための価格というのは

実勢価格ではない。

相続税を計算する為の価格というのは

低くなりやすいんですね。

要は今売ったら

5000万円の価値が有る

家だったとしても

相続税の計算時には

5000万円にはならない

という事です。

・建物

・土地

それぞれの価格だったり。

なので買った時

5000万円の不動産を

相続したんだから

即座に相続税がかかる

という事ではないんですね。

不動産はそういうものだと

覚えておいてもらえればいいです。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

不動産の価値評価には「一物五価」という考え方があります。これは、同じ不動産でも5つの異なる価格が存在することを示しています。具体的には、公示価格、基準値標準価格、路線価、固定資産税評価額、実勢価格があります。実勢価格は一般的に最も高くなる傾向がありますが、相続税の計算には実勢価格ではなく、他の評価方法が用いられることが多いです。

不動産の評価は、土地と建物を分けて行います。土地は損耗しない一方、建物は使用年数とともに損耗します。したがって、減価償却の対象となります。土地の評価は路線価や固定資産税評価額に基づき、建物も固定資産税評価額に基づいて行われます。これらの評価額は、実際の売買価格とは異なることが多いです。

例えば、5000万円で購入した不動産でも、相続税の計算時にはその価格に達しないことがあります。したがって、不動産の購入や相続の際には、これらの評価方法を理解することが重要です。

Citations:

[1] https://www.re-guide.jp/assess/docs/appraisal/

[2] https://realestate-od.jp/realestate/column/article137/

[3] https://ogakan.com/column/269.html

[4] https://suumo.jp/baikyaku/guide/entry/fudosan_hyokagaku

[5] https://ap.betsudai.jp/column/column9.php

[6] https://www.livable.co.jp/solution/brand/contents/211223-1.html

[7] https://nakajitsu.com/column/66947p/

[8] https://landnet.co.jp/redia/14994/

[9] https://www.rehouse.co.jp/relifemode/column/at/at_0186/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Discussion~

【Real Estate Value: It’s Not Just One—Understanding the ‘Five Prices’ Concept】

The method of valuing real estate involves separating the assessment of:

– Land

– Building

Land Valuation

Land is evaluated based on:

– Road Price (Rosenka)

– Fixed Asset Tax Value

Note: These are not based on the actual sale price.

Building Valuation

Similarly, buildings are evaluated based on the Fixed Asset Tax Value, not the actual sale price.

Just because you bought a house for 50 million yen doesn’t mean the property is automatically worth 50 million yen.

Why separate land and building valuations?

The reason is that buildings depreciate over time, while **land does not.

– Land: Even after 30 years, land doesn’t wear out.

– Building: After 30 years, buildings tend to deteriorate and lose value.

Additionally, whether depreciation applies is an important point. For example, if a building is upgraded, its value could change.

Therefore, you need to treat land and buildings separately to calculate the value correctly.

Remember the “Five Prices”

Do you remember the concept of “Five Prices” from past real estate investment discussions?

Real estate, as a physical object, has **five different values**:

1. Official Price (Kouji Kakaku)

2. Standard Base Price (Kijunchi Hyoujun Kakaku)

3. Road Price (Rosenka)

4. Fixed Asset Tax Value

5. Market Price (Actual Sale Price)

The Market Price is the price at which the property is typically bought and sold.

In many cases, the Market Price is the highest.

Important Note on Inheritance Tax

When calculating inheritance tax, the Market Price is not used. Instead, the price for inheritance tax purposes is usually lower.

For instance, even if the market value of your house is 50 million yen when you sell it, it will not be considered as 50 million yen when calculating inheritance tax.

Summary

– The value of land and building are evaluated separately.

– Just because you bought a property for 50 million yen doesn’t mean the inheritance tax will be based on that amount.

– Real estate has multiple values, and it’s important to understand these differences when dealing with taxes or investment decisions.

Special Thanks OpenAI and Perplexity AI, Inc