「一緒にしない|Mixing is Dangerous!」

今日は【貯める力】

養老保険をおすすめしない理由

についてお話しします。

●保険は守るもの、投資は増やすもの~混ぜるなキケン~

知り合いが相談を受けたそうです。

「積立型の投資は不要だとお話されてますよね?

養老保険についてはどうでしょう?

投資と違い元本は保証されています。

万が一の際には保険も下りて

元本保証もあって

貯金も出来るという考えはどうでしょうか?」

とのこと。

このケースについてお話します。

結論としては

いりません。

不要です。

私はやらないですし人にも勧めません。

「どう?」

と聞かれたら

いらないと即答します。

保険は保険

投資は投資

混ぜるなキケン!

これはずっとお話ししてきました。

一緒にしないというのが大切です。

●死亡保障が欲しい?投資で増やしたい?~それなら、それぞれ別で考えましょう~

養老保険がいらない理由ですが

ずっとお話ししてきている

生命保険の話と一緒ですね。

養老保険とは?

保証と貯蓄がセットになった保険です。

もう少し解説すると

生命保険のうち

一定の期間を定めたもので

満期時に

満期保険金が支払われる保険

という事です。

具体例をお話しします。

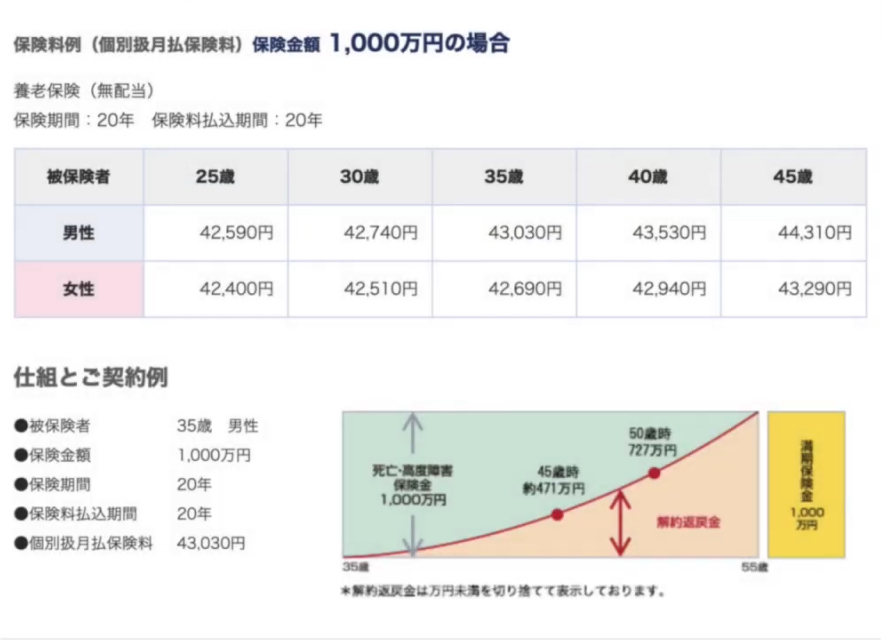

(出典 ソニー生命)

30歳で加入して

年間保険料が52万円とします。

(43,030×12=516,360)

年間保険料を52万円払って

20年間払い続けたとします。

そうすると

死亡保証が1000万円付く保険です。

(516,360×20=10,327,200)

もしも30〜50歳までの間に

亡くなってしまったら

1000万円もらえるんですよ。

例えば

今年払い始めて

来年亡くなってしまっても

死亡保証1000万円もらえる

保証がついてるということですよね。

50歳になって生きていても

1000万円もらえる。

生きてても1000万円

途中で亡くなっても1000万円

セールストークとしては

「払った保険料が無駄になりません!」

みたいなことを言う訳ですよね。

万が一の時の保証を確保しつつ

教育資金とか老後資金を

貯めたいという人に

人気が有るんですよね。

だから

積立型の保険はいらないという

お話しをすると

「いやいや投資に回したら

途中で損するかもしれないじゃないか!」

ということに加えて

「保険だったら途中で亡くなっても

保障が付いてるじゃないか!」

という意見を言ってくる人がいます。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

養老保険をおすすめしない理由について説明します。まず、保険と投資は別々の目的を持つものとして考えることが重要です。保険は万が一の際に備えるためのものであり、投資は資産を増やすためのものです。これらを混ぜると、目的が曖昧になり、リスクが増大します。

養老保険は、死亡保障と貯蓄がセットになった商品です。例えば、30歳で加入し、年間52万円の保険料を20年払うと、死亡保障として1000万円が付く保険です。50歳になっても生きていれば1000万円が支払われます。セールストークでは「払った保険料が無駄にならない」と強調されますが、実際には保険料が高く、他の投資に回す方が効率的です。

また、養老保険は元本保証があるため安全に見えますが、インフレリスクや金利リスクも存在します。投資に回すことで、より高いリターンが期待できます。ただし、リスクも高くなるため、自分で判断して選択することが重要です。複雑な商品や理解できないものには投資しないことが賢明です。

結論として、保険は保険として、投資は投資として明確に分けて考えることが推奨されます。養老保険は不要であり、他の投資先を検討する方が良いとされています。

Citations:

[1] https://adviser-navi.co.jp/watashi-ifa/column/13592/

[2] https://www.acn-fudosan.co.jp/column/archives/122

[3] https://www.meijiyasuda.co.jp/find2/light/knowledge/list/61.html

[4] https://www.meijiyasuda.co.jp/find2/light/knowledge/list/10.html

[5] https://my-best.com/articles/411

[6] https://www.f-l-p.co.jp/knowledge/46776

[7] https://www.manulife.co.jp/ja/individual/about/insight/column/article/column114.html

≪≪Chat-GPTくんによる英訳≫≫

Today, I will talk about the “Power of Saving” and why I do not recommend Endowment Life Insurance.

【Insurance is for protection, investment is for growth—Don’t mix them!】

A friend of mine recently received a consultation. They were asked:

“You’ve said that積立型 (systematic investment) is unnecessary, but how about Endowment Life Insurance?

Unlike investments, it guarantees the principal. And in case of an emergency, it provides both life insurance and principal protection while allowing you to save—what do you think about that idea?”

Here’s the conclusion:

It’s unnecessary. I don’t do it and I wouldn’t recommend it to others. If asked, my immediate answer is no.

Insurance is insurance, investment is investment.

Don’t mix them! I’ve been saying this all along. It’s important to keep them separate.

【Want death benefits? Want to grow your investment?—Then let’s consider them separately.】

The reason I don’t recommend endowment insurance is because it’s essentially the same as what I’ve been talking about regarding life insurance.

So, what is Endowment Life Insurance?

It’s insurance that combines both protection and savings.

To explain further, it’s a type of life insurance with a fixed period, and upon maturity, the sum of the policy is paid out.

Let me explain with a specific example.

(Source: Sony Life Insurance)

Let’s say you enroll at 30 years old, and your annual premium is 520,000 yen (43,030 × 12 = 516,360).

You continue to pay this 520,000 yen for 20 years.

After 20 years, you would have a life insurance policy with a death benefit of 10 million yen (516,360 × 20 = 10,327,200).

If you pass away between 30 to 50 years old, your beneficiaries will receive 10 million yen.

For example, if you start paying this year and pass away next year, your beneficiaries will still receive the death benefit of 10 million yen.

Even if you reach 50 and are still alive, you still get the 10 million yen.

Whether alive or deceased, you get the 10 million yen.

A common sales pitch for this product is:

“Your premiums won’t go to waste!”

It appeals to people who want to secure death benefits while saving for things like education or retirement funds.

So, when I tell people that savings-based life insurance isn’t necessary, I often hear:

“But if I invest, I might lose money along the way!”

And they also say:

“Isn’t life insurance good because it guarantees payment even if something happens in the middle?”

These are some of the typical responses.

Special Thanks OpenAI and Perplexity AI, Inc