「意味無いですよね?|永遠のテーマ、賃貸 vs 持ち家―未来への投資を考える」

〜前回のつづき〜

⚫︎家選びは“価格”ではなく“価値”で決まる~買った瞬間に損をしない家を選べていますか?~(つづき)

では30年後ならどうなるのか?

だいぶ話が

ややこしくなるんですけど

30年後だったら家賃分お得では?

という事になるんですけど

「家賃を払った分

自分の家になりますよ!」

不動産屋の

魔法のワードですよね?

実際にはすぐ売って

2千万円の価値しか無い物件を

3千万円で買ってしまった場合

これは負債になる。

しかも

年々価値は下がっていく訳ですよね?

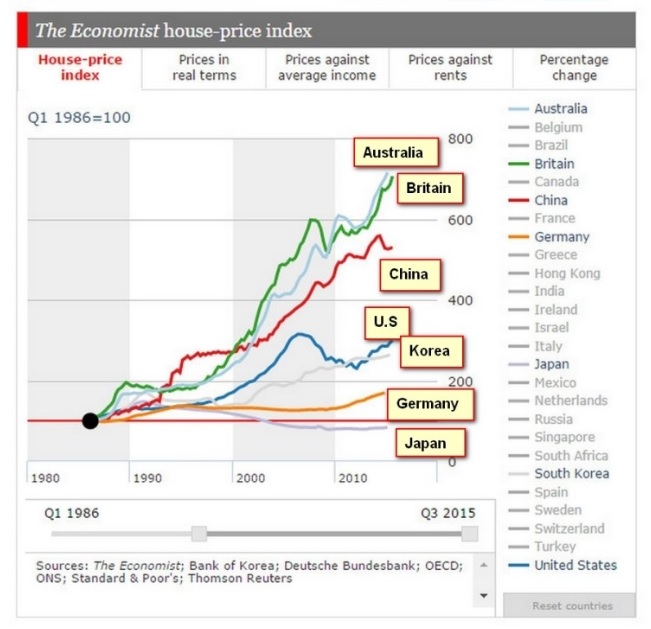

(出典:https://www.facebook.com/TheEconomist/photos/dailychart-the-economist-house-price-index-tracks-the-health-of-housing-in-26-ma/10153220443804060/)

しかし海外では

上がっていく傾向にあります。

日本以外の国では

大体上がり続けます。

ほとんどの家は

価格以下の価値しか無い家です。

なので

いくら自分のものになったとしても

割高な買い物してたら

意味無いですよね?

家賃7万円の価値の家に

わざわざ10万円で住むみたいな

感じになっちゃう。

例えば

賃貸で住んだ場合

30年間の家賃総額が

3,500万円だったとします。

持ち家の場合

3,000万円で買った家が

35年後売値が500万円になった。

という事は

2,500万円値下がりしてるので

2,500万円で住めた

という事になりますよね?

賃貸に住んでたら3,500万円

総額家賃を払った

という事になります。

持ち家の場合だったら

実質2,500万円で住めた。

「ということは持ち家の方が

1,000万円得じゃないか!」

という話だと思うんですけど

持ち家の場合というのは

購入価格以外にかかる費用が

すごく大きいんですね。

最初の方でもお話ししましたが

持ち家の場合は購入価格に加えて

ローンの金利ですよね?

3,000万円の家で

仮に1%の金利で35年だったら

600万円ぐらい払うんですよね。

この金利って

「1%だから安いな」

と思うかもしれませんが

結構負担大きいんですよ。

金利の変動とかがあったとしたら

もっと負担が膨らんでいく。

それ以外にも

・保険

・固定資産税

・修繕費

などです。

・水まわり

・外壁

・床

など大きいところを何年かに一度

修繕しなければならない。

35年間何も直さずにいける

という事はありません。

修繕費って

大体1,200万円ぐらい

使うそうなんですけど

持ち家の場合は

3,000万円で買った家の場合でも

・金利

・修繕費

・固定資産税

などがかかります。

固定資産税なんかは

大体5,000万円かかる。

賃貸であれば

・火災保険料

・更新料

などタカが知れてます。

ほぼ家賃だけ払うことになる。

前提条件は無数に有りますが

この例で言えば35年で

持ち家の場合は

実質5,000万円払って

500万円の家が残り

4,000万円の住居費が掛かった

という事になります。

賃貸の場合であれば

3,500万円払って

家は残らないけど

住居費は安く済んだ。

4,500万円と3,500万円の住居費

どっちが得だったのか?

という話です。

そこに加えて持ち家の場合は

様々なリスクがありますよね?

ということで

もちろん前提条件がすごく多いので

一概には比べる事は出来ません。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

家選びでは「持ち家」と「賃貸」のどちらが得かを判断する際、費用や価値の変動、リスクを考慮する必要があります。

持ち家は購入費用に加え、住宅ローン金利、修繕費、固定資産税などがかかり、日本では住宅価値が下がる傾向があるため、総額が割高になる場合があります。一方で資産として残る可能性や制度的メリットがあります。

一方、賃貸は初期費用やランニングコストが抑えられ、自由度が高いものの、家賃は掛け捨てとなり資産形成には繋がりません。例えば35年で持ち家の住居費が4000万円、賃貸が3500万円だった場合、賃貸の方が安く済むこともあります。

どちらを選ぶかはライフスタイルや経済状況に応じた判断が必要です。

Citations:

[1] https://renoduce.com/media/second-hand-apartment/rent-owner-comparison/

[2] https://ishinhome.co.jp/column/2024/04/1899/

[3] https://www.mitsuba-h.com/mochiie_chintai/

[4] https://www.livable.co.jp/l-note/question/g15530/

[5] https://www.toho-machida.co.jp/thanks/?ct_5bJad1ww470086ef=13.8.365.4332d085J26U6J93.365.Vf364f5B35d735VE9260B9E0.39O36tleCtUOlC620e4397Uu.null

[6] https://diamond.jp/articles/-/343370

[7] https://suumo.jp/article/oyakudachi/oyaku/sumai_nyumon/hikaku/140730_1/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Discussion~

【Choosing a Home Based on “Value” Rather Than “Price” – Are You Selecting a Home That Won’t Lose Value the Moment You Buy It? (Continued)】

What Happens After 30 Years?

The discussion becomes quite complex at this point.

Some might argue, “Won’t owning a home be more cost-effective than paying rent for 30 years?”

Real estate agents often use the magical phrase:

“The rent you pay turns into your own home!”

However, if you buy a house for 30 million yen, but its actual value is only 20 million yen, that difference becomes a financial burden.

Moreover, in Japan, property values tend to decrease over time.

Property Prices Tend to Increase Overseas

Unlike Japan, in many other countries, property prices generally appreciate.

Most houses in Japan have a lower actual value than their purchase price.

Even if you own the property, if you overpaid for it, there’s little financial benefit.

It’s like renting a house worth 70,000 yen for 100,000 yen per month—essentially an overpriced deal.

Comparing Renting vs. Owning Over 30 Years

Let’s assume:

– Renting: Total rent paid over 30 years = 35 million yen

– Owning: Purchased for 30 million yen, but after 35 years, it sells for only 5 million yen

– The property loses 25 million yen in value, meaning the actual living cost is 25 million yen

At first glance, homeownership seems like a 1 million yen saving compared to renting.

However, owning a home comes with additional expenses beyond the purchase price:

– Loan Interest: For a 30 million yen home with a 1% interest rate over 35 years, you’d pay around 6 million yen in interest.

– Property Taxes

– Insurance

– Repair & Maintenance Costs

Large-scale repairs (plumbing, exterior walls, flooring) are necessary every few years.

It’s unrealistic to assume a house can go 35 years without any maintenance.

Total Costs Over 35 Years

Homeownership:

– 30 million yen (purchase price)

– 6 million yen (loan interest)

– 12 million yen (maintenance costs)

– 5 million yen (property taxes)

– Total: 50 million yen

– House value left: 5 million yen

– Net housing cost: 40 million yen

Renting:

– Total rent paid: 35 million yen

– No remaining property value

– Net housing cost: 35 million yen

Conclusion

Renting costs 35 million yen, while owning costs 40 million yen—which is actually more expensive.

Additionally, homeownership carries risks such as:

– Declining property value

– Unexpected repair costs

– Loan interest fluctuations

Of course, the actual comparison depends on various factors, so it’s impossible to make a universal judgment.

Special Thanks OpenAI and Perplexity AI, Inc