管理人オススメコンテンツはこちら

「精神的にものすごくいい|繰下げ受給で得する老後設計!100歳まで安心の資金計画」

〜前回のつづき〜

●オススメは資産運用じゃなくて・・・

貯金からの繰下げ受給というのを

オススメしたいんですね。

繰下げ受給というのをすると

最大で年金の受給額は

184%になるんですよ。

シミュレーションで説明しますね。

前提として

年齢:65歳

貯金:2千万円

年金:夫婦で年間250万円

支出:350万円

ケース(1)

65歳から年金を受給する場合

毎年100万円の赤字が出るんですよ。

毎年生活費で350万円必要なのに

年金は250万円だからですよね。

そうすると

段々貯金が減っていく訳ですよね?

もらえる年金よりも

出ていく生活費の方が大きいんだから

毎年毎年お金が出ていきますよね?

こうなると

85歳で貯金が尽きるんですよ。

男性の平均寿命は81歳

女性は87歳と言われてるんですけど

人生100年時代になってきてるので

若干不安が残りますよね?

『長生きリスク』という事です。

ケース(2)

70歳から年金を受給する場合

65歳〜69歳の5年間

年金を受給せずに

貯金だけで乗り切ることになるんですね。

その場合5年で

貯金残額が250万円になるんですよ。

2千万円持ってるところを

生活費で350万円毎年使う訳ですよね?

これを5年間使ったら

1750万円使う訳ですね。

2000万円-1750万円=250万円

そして70歳になったタイミングで

毎年350万円の年金を受給するんですね。

毎年250万円もらえる予定だった年金が

70歳から受け取る事によって

142%になるので

250✖️1.42=355万円

受け取ることになります。

わかりますか?

本来であれば

250万円受け取る事が出来たところを

70歳に繰下げする事で355万円

毎年年金がもらえるようになるんですね。

そうすると毎年の収支が

プラスになるんですよね。

85歳で貯金325万円という事です。

生活費年間350万円

年金355万円

差額5万円✖️15年=75万円

70歳時点での貯金250万円なので85歳で

75万円+250万円=325万円

となる訳です。

毎年の収支がプラスになるんですよ。

だから100歳まで生きても

余裕という事ですね。

減らないというのが

精神的にものすごくいい。

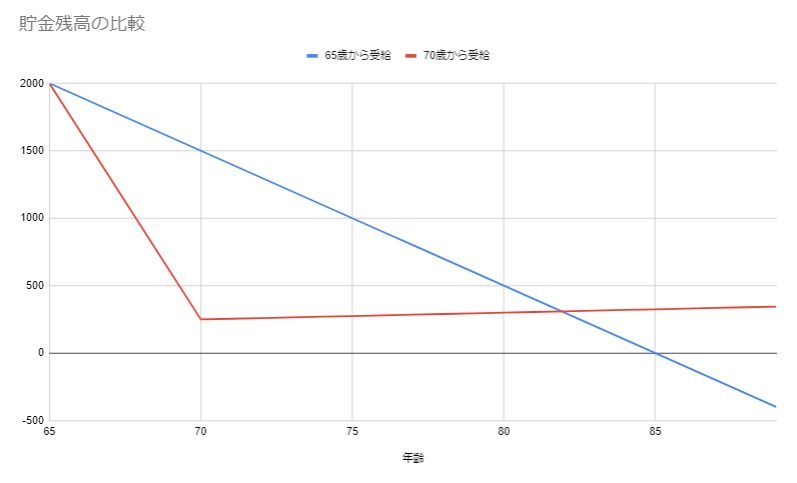

グラフで視覚的に比較するとわかりやすい。

青い線が65歳から受給した場合。

収支がマイナスなので

毎年毎年貯金がずっと減っていっちゃう。

70歳から受給すると

年金がもらえない65〜69歳までの間は

貯金を食いつぶすので

減っていってしまうんですけど

70歳地点からは

プラスに転じて

ずっと増えていくんですよね。

という事で長生きすればするほど

このケースでいうと

70歳から受給した方がお得

という事になるんですよね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

年金の受給方法について、65歳から受給するケースと70歳から受給するケースを比較したシミュレーションがあります。

まず、65歳から年金を受給すると、年間250万円の年金に対して生活費が350万円かかるため、毎年100万円の赤字が出ます。この結果、85歳までに貯金2000万円が尽きてしまい、長生きリスクが懸念されます。

一方、70歳から年金を受給する場合は、65〜69歳の5年間を貯金で賄います。この期間に1750万円を使用し、70歳時点で250万円の貯金が残ります。70歳からは年金が142%に増加し、年間355万円を受け取れるため、毎年の収支がプラスになります。85歳時点では貯金が325万円に増え、100歳まで安心して生活できる見込みです。

このように、繰下げ受給は年金額を大幅に増やし、長生きリスクにも対応できるため、精神的にも安心感があります。視覚的なグラフでも、この違いは明確に示されます。

Citations:

[1] https://www.saisoncard.co.jp/topic/entry/sin_nisa_2311/

[2] https://www.resonabank.co.jp/kojin/column/shisan_kihon/column_0020.html

[3] https://money-bu-jpx.com/news/article017403/

[4] https://president.jp/articles/-/75252

[5] https://www.aeonbank.co.jp/investment/special/076/

[6] https://media.moneyforward.com/articles/8777

[7] https://president.jp/articles/-/75199?page=1

[8] https://media.moneyforward.com/articles/8777/summary

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【The recommendation is not asset management…】

What I want to recommend is delaying pension payments and using savings in the meantime.

By deferring pension payments, you can increase your pension by up to 184%.

Let me explain this through a simulation.

First, here are the assumptions:

- Age: 65

- Savings: 20 million yen

- Pension: 2.5 million yen per year (for a couple)

- Expenses: 3.5 million yen per year

Case (1)

If you start receiving your pension at age 65, you will incur a yearly deficit of 1 million yen.

You need 3.5 million yen for living expenses each year, but your pension income is only 2.5 million yen.

So, naturally, your savings will gradually decrease.

Since your expenses are larger than your pension income, you’ll be drawing from your savings every year.

In this scenario, your savings will be depleted by the time you turn 85.

The average life expectancy for men is 81 years, and for women, it’s 87 years.

However, as we enter the era of living to 100 years, there’s some uncertainty here.

This is referred to as the “longevity risk.”

Case (2)

If you delay receiving your pension until age 70, you would need to rely solely on your savings from age 65 to 69.

In this case, after 5 years, your remaining savings will be 2.5 million yen.

You start with 20 million yen and spend 3.5 million yen each year for living expenses.

After 5 years, you’ll have spent 17.5 million yen.

So, 20 million yen – 17.5 million yen = 2.5 million yen.

At age 70, you will begin receiving a pension of 3.55 million yen annually.

The pension, which was originally supposed to be 2.5 million yen annually, will increase to 142% by deferring it until age 70.

Thus, 2.5 million yen × 1.42 = 3.55 million yen.

Do you understand?

By delaying your pension until age 70, you will receive 3.55 million yen annually instead of the original 2.5 million yen.

This means your yearly balance will become positive.

By age 85, you’ll still have 3.25 million yen in savings.

Your annual expenses are 3.5 million yen, and your pension will be 3.55 million yen.

The difference is 50,000 yen per year, and over 15 years, this adds up to 750,000 yen.

Since you had 2.5 million yen in savings at age 70, by age 85:

750,000 yen + 2.5 million yen = 3.25 million yen.

In other words, your yearly balance becomes positive.

This means that even if you live to 100 years old, you’ll still have financial security.

Not having to worry about your savings decreasing provides great peace of mind.

When you look at a graph, it becomes even clearer.

Visually comparing the two cases makes it easy to understand.

In the graph, the blue line represents starting pension payments at age 65.

Because your balance is negative, your savings keep decreasing year after year.

On the other hand, if you start receiving your pension at age 70, your savings will decrease from age 65 to 69 as you rely on them for living expenses.

However, once you reach age 70, your balance turns positive, and your savings begin to increase.

In conclusion, the longer you live, the more advantageous it is to defer your pension until age 70.

Special Thanks OpenAI and Perplexity AI, Inc