管理人オススメコンテンツはこちら

「死に金|個人年金保険の真実、知っていますか?」

〜前回のつづき〜

●個人年金保険の利回りの計算方法(つづき)

「利回りが高いと思うんですけど」

という人はここが間違いなんです。

こういう考え方をしてるんですね。

この計算方法で考えてるという事が

間違いなんですよ。

これは

「複利で計算されてない」

んですよ。

ここです。

多くの人が見落としてるポイントです。

かなりの人が見落とすのが普通なので

よく聞いておいてほしいんですけど

節税効果が有るのは

保険料を支払った年のみなんですよ。

1年目のみ。

わかりますか?

ポイントはここなんですよ。

つまり1年目に支払った12万円には

6,800円の節税効果が

確かに有るんですよ。

確かに有るんですけど

2年目の時点では1年目に支払った保険料には

節税効果が無いんですよ。

何も生み出さない。

1年目に支払った12万円が

死に金になってるという事です。

保険料というのは

累計で見ていくべきなんですよ。

要するに

累計でどんなに沢山の

保険料を支払っていたとしても

毎年の節税額は

ロックされてるんですね。

時間が経てば経つほど

もう既に過ぎた年度に支払った

死に金というのが累積していく。

そうなると

単年度の利回りは

低下していくんですね。

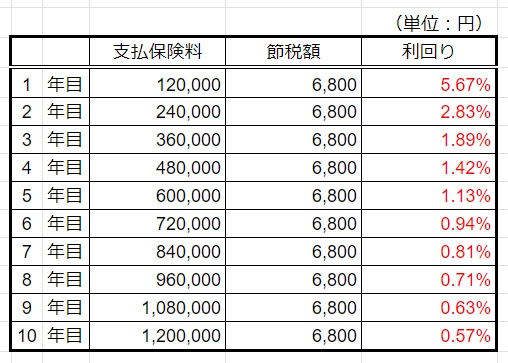

(個人年金保険の利回り 修正後)

こっちが正しい計算方法なんですよ。

さっきので言うと

1年目はロックされてる。

この支払い保険料というのは

累積していってるので

この場合だったら

実際の利回りは0.57%な訳ですよ。

1年目だけ5.67%で

年間ずっとトータルで見ていくと

ドンドンドンドン利回りは落ちていく。

「では最初の方に

解約したらいいんじゃないのか?」

という話も

出てくるかもしれないですけど

屁理屈をこねると

「新規契約して

すぐ節税効果をゲット!

翌年解約して新規契約。」

これを繰り返せば

毎年5.67%の利回りを

維持出来るんですけど

しかし解約したら

1年経った時点で

元本割れする訳ですよ。

だからこんな事は通常できない。

だから時間単価も低くなるし。

1年間掛けて契約したり解約したり

色んな事をしている間に6,800円だけ。

自分の時間はタダじゃない。

自分の時間給から考えたら

すぐに損しちゃうという事ですよね。

それに大体が解約すると

すぐに元本割れしますしね。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

個人年金保険の利回り計算について、多くの人が陥りやすい誤解を解説します。一般的に高い利回りと思われがちですが、実際はそうではありません。最大の誤りは、複利計算を考慮していないことです。

重要なポイントは、節税効果が保険料支払い年のみに適用される点です。つまり、1年目に支払った保険料には確かに節税効果がありますが、2年目以降はその効果がなくなります。時間が経つにつれ、過去に支払った保険料は「死に金」となり、単年度の利回りは低下していきます。

正しく計算すると、実際の利回りは最初の年よりも大幅に低くなります。例えば、1年目は5.67%の利回りでも、年数が経つにつれて0.57%程度まで下がる可能性があります。

毎年新規契約と解約を繰り返せば高い利回りを維持できるという考えもありますが、解約時の元本割れや時間のコストを考えると現実的ではありません。個人年金保険の利回りを評価する際は、長期的な視点で複利効果を考慮することが重要です。

Citations:

[1] https://www.hokende.com/life-insurance/pension/basic_info/select_return_rate

[2] https://money-career.com/article/636

[3] https://www.f-l-p.co.jp/knowledge/62957

[4] https://life.insweb.co.jp/nenkin/yotei-riritsu.html

[5] https://www.d-frontier-life.co.jp/products/index_choice.html

[6] https://hoken-room.jp/pension/11666

[7] https://www.daiwa.jp/lp_dc/ideco/column/article_130/

[8] https://www.jili.or.jp/knows_learns/q_a/tax/568.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【How to Calculate the Yield of a Personal Pension Insurance (Continued)】

“You might think the yield is high.”

But this is where the mistake lies.

People are using this kind of thinking.

The issue is that this calculation method is wrong.

It’s because…

“It’s not calculated using compound interest.”

This is the key point.

Many people overlook this.

It’s common for a lot of people to miss this, so please pay attention.

The tax-saving benefit only applies to the year when the premium is paid.

Only in the first year.

Do you understand?

This is the key point.

In other words, the 120,000 yen paid in the first year does have a tax-saving effect of 6,800 yen.

It certainly does, but by the second year, the premium paid in the first year no longer has any tax-saving effect.

It produces nothing.

The 120,000 yen paid in the first year has essentially become “dead money.”

You need to look at the premium cumulatively.

No matter how much you pay in total premiums over the years…

The yearly tax-saving amount is locked in.

As time passes, the premiums paid in previous years accumulate as dead money.

As a result, the annual yield decreases.

(Corrected Yield of Personal Pension Insurance)

This is the correct calculation method.

As I mentioned earlier, the first year is locked in.

The premiums are accumulating, so…

In this case, the actual yield is 0.57%.

The first year’s yield is 5.67%, but when you look at the overall yearly total, the yield keeps dropping.

“Then, wouldn’t it be better to cancel early on?”

You might think this, but I’ll address this later, so please listen for now.

If we twist the logic, you could say:

“Sign a new contract, immediately get the tax benefit, cancel next year, and then sign a new contract.”

By repeating this, you could maintain a 5.67% yield every year.

But if you cancel after a year, you’ll face a loss of principal.

So, this kind of strategy is not practical.

It also reduces the value of your time.

If you spend a year signing and canceling contracts, you’d only get 6,800 yen in return.

Your time isn’t free.

When you think about your hourly rate, you’re losing money quickly.

And usually, canceling leads to an immediate loss of principal.

Special Thanks OpenAI and Perplexity AI, Inc