管理人オススメコンテンツはこちら

「IRR(内部収益率)|保険の利回り、実はこう計算できる!」

〜前回のつづき〜

●知っておこう!正しい計算方法

ではどうすれば

保険について正しい計算方法で

利回りが出せるのか?

保険屋さんというのは

都合の悪い数字というのは

絶対に出さない。

これはここがポイント。

この言葉ですよ。

『IRR: Internal Rate of Return(内部収益率)』

この言葉を覚えておいてほしいです。

専門用語っぽくて嫌ですよね?

「もうーおぼえらんない!」

「横文字キライ!」

みたいな。

概念というのは

もう説明しないので

計算方法だけ覚えてください。

とりあえずIRR=複利と

思ってもらえれば

それでいいです。

これだけで計算出来る。

計算方法は非常に簡単なので

言葉だけで嫌にならずに

是非覚えて欲しいんですよ。

まずExcelを準備してください。

Googleスプレッドシートでも構いません。

そしてIRR関数を使います。

この2つだけでできます。

さっきの

明治安田生命の個人年金保険というのをベースに

シミュレーションしてみましょう。

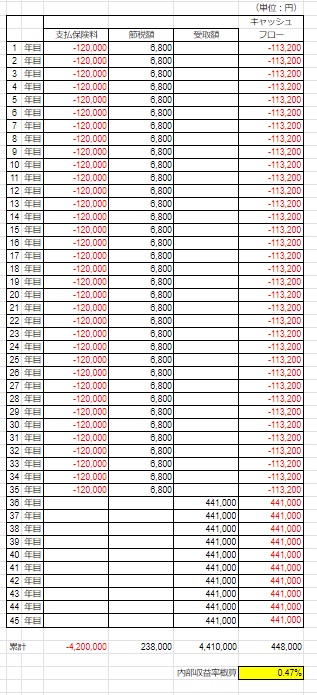

30歳から毎年12万円支払って

毎年の節税額は6,800円。

65歳から10年間

毎年44万円受け取る。

とりあえず計算結果だけを

見てみましょう。

(個人年金保険の利回り)

ザックリこんな感じになるんですよ。

30歳から毎年12万円支払っていって

65歳から10年間

毎年44万円を受け取る。

というと

この商品の最終利回りは

0.47%になるんですよ。

たとえ収入が増えて

節税額というのは増えても

雀の涙なんですよ。

保険料を払ってる期間が35年間で

所得が1,800万円以上の人

所得税率が

非常に高いエリートの人でも

最終的にこのIRRという利回りは

0.96%にしかならないんですよね。

全期間で所得税率20%だと

IRRは0.63%

要はどういう事かというと

普通の所得の人だったら

ちょっとぐらい高くても

せいぜい

0.5%前後の利回りにしか

ならないんです。

年間2千万円くらい貰ってるような

超エリートで

やっと0.96%の効果なんですよ。

それ以外のほとんどの人は

0.5%に満たないぐらいしか

実際の複利では

回らないという事です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

個人年金保険の利回りを正しく理解するためには、IRR(内部収益率)を用いることが重要です。この指標は、ExcelやGoogleスプレッドシートのIRR関数を使って簡単に計算できます。例えば、30歳から毎年12万円を支払い、65歳から10年間毎年44万円を受け取るケースを考えると、一般的な所得の人は利回りが約0.5%程度となります。一方、高所得者(年収1,800万円以上)でも最終的な利回りは0.96%にとどまります。節税効果を考慮しても、多くの人にとって個人年金保険の実質的な利回りは1%未満です。このことから、個人年金保険の投資効率が低いことが明らかであり、加入を検討する際には慎重な判断が求められます。

Citations:

[1] https://va-dmn2.nissay.co.jp/vkhengaku/servlet/JP.co.nissay.KE8.KE8S008Z

[2] https://hoken-room.jp/student/5721

[3] https://www.aflac.co.jp/soudan/guide/contents/application/productcreditingrate.html

[4] https://www.hokende.com/life-insurance/pension/basic_info/select_return_rate

[5] https://www.meijiyasuda.co.jp/norapl/find/rate/dolcommon/planned_interest_rate/

[6] https://www.daiwa.jp/lp_dc/ideco/column/article_130/

[7] https://selfs.dai-ichi-life.co.jp/apl/menu/service?ZEC_EPCD=M6B262R7UU&ZEC_GRP=C0&_PAGEID=ZEA_INITIAL_PAGE&_TRANID=ZEMNewSim11P00

[8] https://www.fukoku-life.co.jp/gakushi/trivia/trivia26/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【Know this! The correct calculation method】

So, how can we calculate the return on insurance accurately?

Insurance agents never disclose inconvenient numbers.

This is the key point.

The term you need to remember is this:

“IRR: Internal Rate of Return.”

I know it sounds like a technical term, right?

“I can’t remember it!”

“I hate fancy terms!”

Something like that.

I won’t explain the concept any further, just remember the calculation method.

For now, just think of IRR as compound interest, and that’s enough.

With this, you can calculate it.

The calculation method is very simple, so don’t get discouraged by the terms and make sure to learn it.

First, get Excel ready. Google Sheets works too.

Then, use the IRR function.

That’s all you need.

Let’s simulate it based on Meiji Yasuda Life’s individual pension insurance.

You pay 120,000 yen every year starting at age 30, and the annual tax saving is 6,800 yen.

From age 65, you receive 440,000 yen annually for 10 years.

Let’s just look at the calculation results.

(The return on individual pension insurance)

It goes something like this:

You pay 120,000 yen every year from age 30 and receive 440,000 yen annually for 10 years starting at age 65.

In this case, the final return on this product is 0.47%.

Even if your income increases and your tax savings go up, it’s still a drop in the bucket.

If you pay premiums for 35 years and earn more than 18 million yen annually, even for high-income earners with high tax rates, the final IRR return is only 0.96%.

If your income tax rate stays at 20% over the entire period, the IRR is 0.63%.

In other words, for regular-income earners, even if the income is a little higher, the return will only be around 0.5%.

Only super-elite earners, making around 20 million yen annually, can achieve a return of 0.96%.

For most others, the actual compound return will be less than 0.5%.

Special Thanks OpenAI and Perplexity AI, Inc