管理人オススメコンテンツはこちら

「個人年金保険の実質利回りと節税効果の真実|実際の利回りを徹底分析」

〜前回のつづき〜

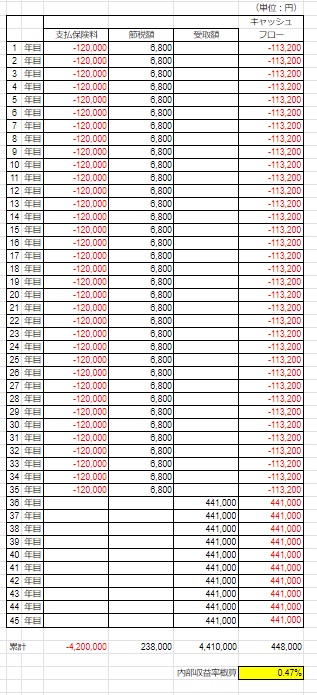

●今まで見てきた個人年金保険の場合はどうなるか?

(1)投資期間 45年

(2)投資期間のキャッシュフローを見る

キャッシュフローというのは

お金の出入りの事だとお話ししました。

(1)投資期間 45年

35年掛けて保険料を払い込む訳ですね。

そして10年かけて年金を受け取る。

合計45年ですね。

キャッシュフローはお金の出入りの事で

出ていくお金というのは保険料。

入ってくるお金というのは

節税額と年金の受給額ですよね?

もらえる金額。

この2つをExcelに打ち込んでいくと

(個人年金保険の利回り)

この表になるんですね。

黄色いセルというのが

このIRR関数のところが

この太枠のところを範囲指定してるだけ。

これはExcelに慣れてる人であれば

すぐにわかってもらえると思うんですよ。

黄色の部分を選択して

IRRという関数を選択するんですね。

関数のところからIRRというのを選んで

太字になってるところを選ぶだけ。

このキャッシュフローとなってる

お金の出入りの合計額のところを選ぶだけ。

そうするとIRRが出るんですよ。

これが節税効果も考慮した

個人年金保険の

本当の利回りになるんですね。

まとめるとこの年金保険は45年の間に

最初の35年で毎年113,200円支払って

これは節税効果を考慮した分ですね。

36年目から10年間で

毎年441,000円受け取る。

純利益は448,000円増えるという

そういう商品で

45年という超長いスパンで

複利はたったの0.47%なんですよ。

0.47%ですよ!

本当にお得な商品だと思いますか?

インフレ率(=物の値上がり)というのを

考慮した時に

自分の資産を守れるような

そういう利回りだと思いますか?

0.47%ですよ!

しかも色んな意味で

資金拘束されるんですよね。

いずれにせよ節税効果で毎年5.67%とか

人によっては7%とか8%の利回りなのと

明らかに全然かけ離れてますよね?

まさに数字のマジック。

保険屋は都合の悪い数字というのは

絶対に言わないんですね。

(保険屋に限らずですけどね)

そういう事を教えてくれない訳ですよ。

なので注意が必要という事ですね。

この節税効果というのは

1年目にしか無いので

だから色んな商品で

ここを考慮してない計算に

なってる事が多い。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

個人年金保険の実際の利回りについての分析を行います。投資期間は45年間で、35年間保険料を支払い、10年間年金を受け取ります。このキャッシュフローをExcelで分析し、IRR関数を使って実際の利回りを算出しました。

結果として、35年間毎年113,200円を支払い、36年目から10年間毎年441,000円を受け取ると、純利益は448,000円増加します。しかし、45年間の複利計算による実際の利回りはわずか0.47%です。この数字はインフレを考慮すると資産を守るには不十分です。

さらに、保険会社が主張する節税効果による5.67%〜8%の利回りとは大きく異なります。節税効果は1年目にしか適用されないため、長期的な視点では影響が限定的です。このように、個人年金保険の実際の利回りは宣伝されているものよりも低く、投資家には慎重な判断が求められます。

Citations:

[1] https://www.dai-ichi-life.co.jp/promotion/stepjump/01/index.html

[2] https://dc.rakuten-sec.co.jp/feature/adults/

[3] https://www.meijiyasuda.co.jp/profile/news/release/2024/pdf/20240828_02.pdf

[4] https://www.fukoku-life.co.jp/ad/miraiplus/

[5] https://www.nissay.co.jp/kojin/lp/nenkin2/

[6] https://www.d-frontier-life.co.jp/products/index_yotei_hendo_kojin_choice.html

[7] https://www.hekishin.jp/column/hoken/61.php

[8] https://www.sonylife.co.jp/land/blog/column001.html

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【What about the individual pension insurance we’ve been discussing so far?】

(1) Investment period: 45 years

(2) Looking at the cash flow over the investment period

Cash flow refers to the inflow and outflow of money.

(1) Investment period: 45 years

You pay premiums for 35 years, and then you receive the pension over 10 years, making a total of 45 years.

In terms of cash flow, the outgoing money is the premium payments, while the incoming money consists of the tax savings and the pension benefits you receive, right?

These are the amounts you get.

When you input these two figures into Excel (for the return rate of the individual pension insurance), you get this table.

The yellow cells are where the IRR function is applied. It simply selects the range marked by the thick borders.

So, anyone familiar with Excel would quickly understand this.

You select the yellow parts and choose the IRR function.

From the list of functions, you select IRR and then choose the bolded range. You just select the total cash flow, which shows the inflow and outflow of money.

This gives you the IRR, which is the actual return rate of the individual pension insurance, considering the tax savings.

To summarize, this pension insurance requires you to pay ¥113,200 annually for the first 35 years (considering the tax savings), and from the 36th year, you receive ¥441,000 annually for 10 years.

This product increases your net profit by ¥448,000, but over a very long span of 45 years, the compound interest rate is only 0.47%.

Just 0.47%!

Do you really think this is a good deal?

When you consider the inflation rate (i.e., rising prices), do you think this is the kind of return that can protect your assets?

It’s just 0.47%!

On top of that, your money is tied up in various ways.

In any case, it’s clearly far from the 5.67% or 7% to 8% annual returns that people think they’re getting due to the tax savings.

This is the magic of numbers.

Insurance companies never reveal unfavorable figures. (This is not limited to insurance companies, of course.)

They don’t teach you these things, which is why you need to be cautious.

The tax-saving effect only applies in the first year, so many products don’t factor this into their calculations.

Special Thanks OpenAI and Perplexity AI, Inc