「ヒドい|数字の裏に潜むリスクを見抜く!賢い投資家の秘訣」

~前回のつづき~

●利回りの魔法に騙されるな~裏にはコスト地獄が潜む~(つづき)

例)

1,000万円で買った物件で

10年間で500万円

家賃が入るとします。

この物件を売った時に

500万円で売れたとします。

もともと

1,000万円有ったのが

500万円で売れただけだったら

結局一緒じゃないですか。

増えてない。

そこも考えないといけない。

なので

表面利回りに騙されてはいけない。

これは

不動産で出てくる用語で

表面利回りという言葉には

気をつけないといけない。

大体マイソク(販売図面)

『表面利回り』と書いてあります。

表面利回りとは何かというと

粗利益のことです。

満室想定の家賃収入を

物件価格で割ったもので

いくらでも高く

見せかける事が出来ます。

例えば

もらえる家賃が年間100万円で

物件価格が1,000万円。

となると

表面利回りは10%になります。

これは満室想定なので

これをチョコチョコっと

100万円を150万円に

書き換えるだけで

表面利回りって

一瞬で15%に増やせるんですよ。

他にも

色々増やす方法はあります。

そうやって

簡単にいじれちゃう。

だからこの実質利回りは

自分で計算しないといけない。

家賃収入から

必要なコストを全部差し引いた

実態を現す利回り。

自分で考えていかないといけない。

だからこのさっきの

表面利回り5.54%というのは

実質の利回りを考えたら

何%になるのか

実際に計算してみたんですね。

ヒドい。

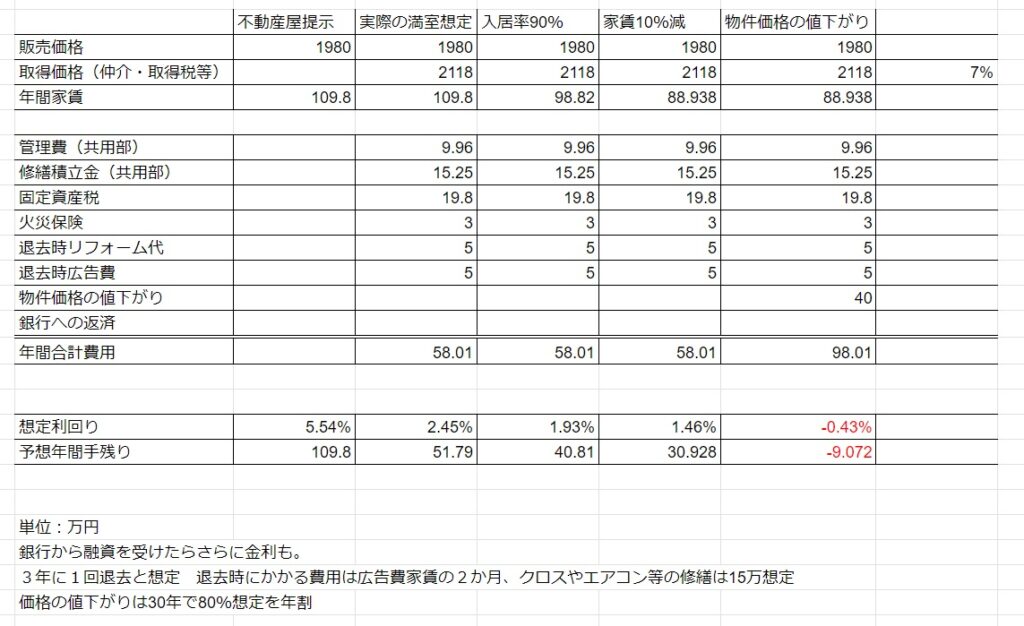

不動産屋が提示している利回りは

5.54%ですよね?

販売価格が1,980万円で

家賃が9.2万円で

それ以外の

・管理費

・修繕積立金

とか全く考えない状態で

予想年間手残りが

110万円まるまる残ると。

それで想定利回りが5.54%。

こんな事ありえないです。

満室想定で出してみました。

販売価格は

1,980万円かもしれませんが

その他に

物件取得価格がかかる。

仲介料と不動産取得税

大体140万円ぐらいかかるんですね。

大体7%ぐらいかかる。

だから2,100万円以上かかる。

それから

・管理費

・修繕積立金

・固定資産税

・火災保険

そういうのを入れていく。

それぐらい入れていくと

想定利回りが

2.45%になるんですよね。

予想年間手残りが

約52万円になる。

これ

全部現金で買った場合

ですからね。

2,118万円

銀行から借り入れせずに

キャッシュで買った場合。

それで

2.45%で52万円ぐらい残る。

これぐらいだったら

銀行に預けておくよりいいかな?と

0.01%金利が付くより

2.4%以上増えるのであれば・・・

と思うかもしれませんが

ちょっと待ってください。

まず入居率ですよね。

空室率というのを

全く考えられてないんですよ。

30年間全く誰も退去せずに

埋まり続ける事はありません。

退去時のリフォーム代とか

退去時の広告費というのは

毎年はかかるものではないですが

一応退去が出るたびにかかります。

数年に一回

掛かってくるものなので

それも年割して大体載せてる。

それで入居率が90%だと。

・10%落ちてしまった場合

・満室じゃなかった場合

30年間ずっと満室なんて

ありえないので

それで計算してみると

年間の家賃が

当然10%下がる訳です。

でもそれ以外は変わらない。

その状態で手残りが

41万円に今度は減った。

これでもいいかなぁって

思う人がいるかもしれませんが

家賃がずーっと同じ価格で

取り続けられる事はまずありません。

30年間家賃が下がらない訳がない。

だって

築15年のマンションが

30年経ったら築45年ですよ。

築45年のマンションを

見てみて欲しいんですけど

結構ボロボロですよね?

その状態で

築10年くらいの時の家賃と

全く同じ価格の家賃を

取れるなんてありえない。

家賃10%落ちたとして

その計算ですると今度は

・想定利回りが1.46%

・手残りが31万円

になってくる。

これでもいいと

言うかもしれませんが

家賃10%で

入居率90%ですからね。

実際には

もっと多分下がってきますね。

家賃10%減じゃ

済まないでしょう。

~~~つづく~~~

Special Thanks college president Ryo.

●おまけ

≪≪perplexityちゃんによる文章まとめ≫≫

不動産投資でよく使われる「表面利回り」は、満室想定の家賃収入を物件価格で割った粗利益であり、実際の利益を示すものではありません。

数字は簡単に操作でき、高く見せかけられるため注意が必要です。実際には購入時の仲介手数料や不動産取得税などの初期費用、毎年発生する管理費や修繕積立金、固定資産税、火災保険料などがかかります。

さらに空室や退去時のリフォーム・広告費、築年数による家賃下落も避けられません。

例えば表面利回り5.54%の物件も諸経費や入居率90%を考慮すると実質利回りは2%台に低下し、手残りも半減します。

家賃下落を加味すればさらに下がります。

投資判断では表面利回りではなく、全コストとリスクを差し引いた実質利回りやキャッシュフローを自分で計算することが重要です。

- https://note.com/humble_heron722/n/n345be892d3ae

- https://note.com/takaoshi/n/n4d05187c112c

- https://note.com/myrealestate/n/n43ba45cce3d2

- https://note.com/unique_abelia393/n/n735bc9480142

- https://note.com/easy_estate/n/n5201bf527800

- https://note.com/navi_fudosan/n/nfbe4f640f5a7

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from last time~

【Don’t Be Fooled by the “Magic” of Yield – Behind It Lurks the Cost Trap (continued)】

Example:

Let’s say you buy a property for 10 million yen, and over 10 years you collect 5 million yen in rent.

When you sell the property, you sell it for 5 million yen.

If you originally had 10 million yen, but you only get back 5 million yen when selling, in the end, it’s the same, isn’t it?

It hasn’t increased.

You have to take that into account as well.

That’s why you must not be fooled by the gross yield.

This is a term you see in real estate, and you have to be careful with the phrase “gross yield.”

Most property listings (sales brochures) have “gross yield” written on them.

So what is gross yield?

It’s basically gross profit — the expected full-occupancy annual rental income divided by the purchase price.

It can be made to look high as much as you like.

For example, if the expected annual rent is 1 million yen, and the purchase price is 10 million yen, then the gross yield is 10%.

But that’s based on full occupancy.

If you just tweak that figure a bit — say, change 1 million yen to 1.5 million yen — the gross yield instantly jumps to 15%.

There are many other ways to inflate it.

It’s that easy to manipulate.

That’s why you have to calculate the net yield yourself — the yield after deducting all necessary costs from the rental income.

You have to think for yourself.

So, taking that earlier example of a gross yield of 5.54%, I calculated what the yield would be when considering the actual net yield.

It was terrible.

The yield presented by the real estate agent is 5.54%, right?

The sales price is 19.8 million yen, with rent at 92,000 yen per month.

And that’s without considering things like:

Management fees

Reserve fund for repairs

In that scenario, they’re claiming the expected annual net income is a full 1.1 million yen, leading to the supposed yield of 5.54%.

That’s impossible.

So I calculated it based on full occupancy.

Even if the sales price is 19.8 million yen, there are acquisition costs.

Brokerage fee and real estate acquisition tax will cost about 1.4 million yen — roughly 7%.

So the total cost is over 21 million yen.

Then you have:

Management fees

Reserve fund for repairs

Property tax

Fire insurance

When you factor those in, the expected yield drops to 2.45%, with the annual net income at about 520,000 yen.

This is assuming you buy entirely in cash.

That’s 21.18 million yen without any bank loan — all paid in cash.

With that, you’re left with about 520,000 yen, or 2.45%.

You might think, “Well, that’s still better than putting it in the bank,” since bank interest is only 0.01% and this is over 2.4% growth…

But wait.

First, the occupancy rate.

They’re not factoring in the vacancy rate at all.

There’s no such thing as 30 years of continuous full occupancy without anyone moving out.

When a tenant moves out, you’ll have to pay for renovations and advertising costs to find a new tenant.

These costs don’t occur every year, but they do come up each time someone moves out — so you need to spread (amortize) those costs over the years.

Let’s say the occupancy rate is 90%.

That means:

A 10% drop in income

Not fully occupied all the time

There’s no way you’ll have 100% occupancy for 30 years.

When you calculate with a 90% occupancy rate, the annual rent naturally drops by 10%.

Everything else remains the same.

In that case, your net annual income drops to 410,000 yen.

Some people might still think that’s fine…

But rental income almost never stays the same over decades.

There’s no way rent stays flat for 30 years.

Think about it — a condo that’s 15 years old will be 45 years old in 30 years.

If you look at 45-year-old condos, they’re often quite worn down, right?

There’s no way you can keep charging the same rent as when it was around 10 years old.

If rent drops by 10%, then…

Expected yield becomes 1.46%

Net annual income becomes 310,000 yen

Some might still say that’s okay…

But that’s with only a 10% rent drop and a 90% occupancy rate.

In reality, it will probably drop more.

A mere 10% rent decrease likely won’t be the end of it.

Special Thanks OpenAI and Perplexity AI, Inc