管理人オススメコンテンツはこちら

「何をやってるんだよ!|未来を売るな!借金ゼロで資産を築く方法」

〜前回のつづき〜

●世論調査のデータで見る『世間一般』と『家計エリート』の違い(つづき)

(3)借入金の状況

.jpg)

(出典:https://www.shiruporuto.jp/public/document/container/yoron/tanshin/2023/pdf/yoront23.pdf)

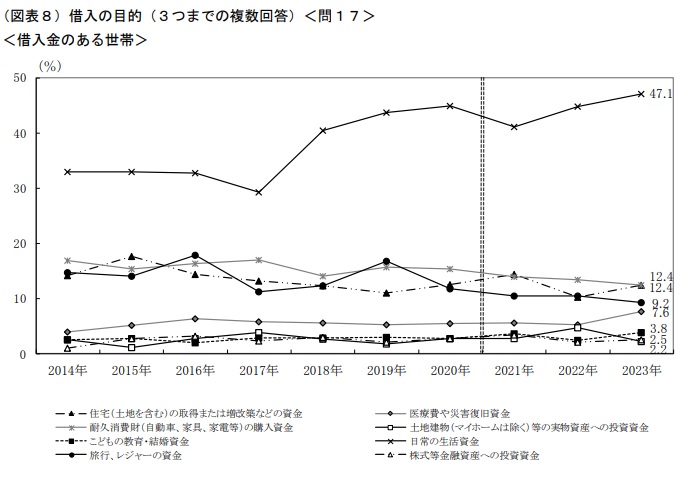

独身世帯の場合は

借入金の有る世帯の割合というのは

12.6%です。

(出典:https://www.shiruporuto.jp/public/document/container/yoron/tanshin/2023/pdf/yoront23.pdf)

そして借入の目的ですが

・日常の生活資金:47.1%

・消費財の購入:12.4%

・レジャー資金:9.2%

という事で

要は5人に1人が

生活費や遊ぶ為のお金を借金している

という事になるんですよ。

なので

・サラ金

・リボ払い

で借りてる人というのが

ほとんどだと思います。

銀行等から事業用にと融資を受けて

生活費に使っているという人は

なかなかいないと思います。

大体

・カードローン

・リボ払い

で借金してる人が多いと思うんですけど

絶対にやめましょう!!

生活費や遊ぶ為のお金を借金してるって

何をやってるんだよ!という話ですよ。

以前にもリボ払いについてのお話しはしました。

↑こちらでお話ししています。

絶対にやめましょう。

当然お金持ちから遠ざかる行為なので

ここからどうやって脱出したらいいか

というのも以前沢山お話ししてるので

読んでみてほしいと思います。

続いて二人以上の世帯の

借入の状況なんですけど

.jpg)

(出典:https://www.shiruporuto.jp/public/document/container/yoron/futari2021-/2023/pdf/yoronf23.pdf)

借入金の有る世帯の割合は

19.4%程度です。

借入の目的は

・住宅の取得:47.4%

・日常の生活資金:22.9%

・耐久消費財:13.7%

という事で

単身世帯の借入目的よりは

マシなんだけど

・住宅ローン

・生活資金

・車、家具、家電等

とかで負債を抱えているという人が

多い事がわかるという。

ここも考えて欲しいですよね?

何のための住宅取得なのかという

そこは考えて欲しい。

これまでも良く話をしてるんですけど

借金というのは言うまでもなく

将来の収入の前借りなんですよ。

なので

自分の未来の時間を

売ってるとも言える。

特に会社員の方の場合は

自分の未来の時間を

先に切り売りしてるんですよ。

しかも高い利息が付く。

今言ったような借金というのは

投資の為の借入と違って

利益を生まないダメ借金なんですよね。

例えば

・車を買う

・家を買う

みたいなの。

ほとんどの方は

・車

・家

といったものに

借金してるみたいなんですけど

これらを投資の為の借入

例えば

1千万円借り入れて

何かに投資するのであれば

利益を生む可能性が

有る訳なんですけど

・車

・家

というのは利益を生んでくれない。

マイホームや車というのは

利益を生んでくれないので

ダメ借金なんですよね。

なのでここは良く考えたいですね。

結論:

家計エリートというのは無借金であり

全体の2〜4割の人は借金を抱えている。

といった感じの状況です。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

世論調査によると、独身世帯の約12.6%、二人以上の世帯の約19.4%が何らかの借入金を抱えています。

独身世帯では、生活費やレジャー資金など消費目的での借金が多く、サラ金やリボ払いを利用するケースが目立ちます。

一方、二人以上の世帯では住宅取得が主な借入目的ですが、生活資金や耐久消費財のための借入も少なくありません。

これらの借金は将来の収入の前借りであり、車や家など利益を生まない「ダメ借金」とされています。

金融リテラシーの高い「家計エリート」は、無借金で家計を管理し、金融資産を着実に増やしていることが特徴です。

全体の2〜4割が借金を抱えている現状を踏まえ、借金に頼らない家計運営の重要性が強調されています

Citations:

[1] https://www.jili.or.jp/lifeplan/houseeconomy/856.html

[2] https://www.shiruporuto.jp/public/document/container/yoron/04-06/2004/04yoron001.html

[3] https://komachi.yomiuri.co.jp/topics/id/1042172/all/

[4] https://www.e-stat.go.jp/stat-search/files?tclass=000000330002&cycle=7&year=20230

[5] https://www.e-stat.go.jp/stat-search/files?page=1&layout=datalist&toukei=00200561&tstat=000000330001&cycle=1&year=20230&month=11010303&tclass1=000000330001&tclass2=000000330004&tclass3=000000330005&result_back=1&tclass4val=0

≪≪Chat-GPTくんによる英訳≫≫

~Continued from the previous part~

【The Difference Between the General Public and Financially Elite Households, According to Survey Data (Continued)】

(3) Borrowing Situations

(Source: https://www.shiruporuto.jp/public/document/container/yoron/tanshin/2023/pdf/yoront23.pdf)

For single-person households,

the percentage of households with debt is 12.6%.

As for the purpose of borrowing:

– Daily living expenses: 47.1%

– Consumer goods: 12.4%

– Leisure expenses: 9.2%

In other words, about 1 in 5 people are borrowing money just to cover living costs or for leisure.

So, it’s likely that:

– Consumer finance companies

– Revolving credit (revolving payments)

are where most of the borrowing is happening.

It’s quite rare to find someone who took out a business loan from a bank and is using it to cover personal living expenses.

Generally, it seems that:

– Card loans

– Revolving payments

are the main methods people use to borrow money—and this needs to stop!

Borrowing money for daily living or leisure is seriously questionable behavior.

I’ve previously discussed the dangers of revolving payments, too.

See:

#17 The Mechanics of Credit and the Nightmare of Revolving Payments – Part 1

I strongly urge you—stop it immediately.

It’s obviously something that pulls you further away from building wealth, and I’ve talked before about how to break free from this trap, so I hope you’ll check those out too.

Now let’s look at households with two or more people.

(Source: https://www.shiruporuto.jp/public/document/container/yoron/futari2021-/2023/pdf/yoronf23.pdf)

The percentage of households with debt is around 19.4%.

The purposes of borrowing are:

– Home purchase: 47.4%

– Daily living expenses: 22.9%

– Durable consumer goods: 13.7%

So, compared to single-person households, the purposes are a bit more reasonable.

Still, many are burdened with debts such as:

– Home loans

– Living expenses

– Cars, furniture, appliances, etc.

This is something we need to think about seriously.

Why are you buying a house in the first place?

This is a question that needs to be asked.

As I’ve said many times, debt is essentially borrowing from your future income.

In other words, you’re selling your future time.

Especially for employees, this means cutting off and selling future time in advance—and with high interest on top.

The kinds of debt mentioned here are bad debt, unlike investment loans that can generate returns.

For example:

– Buying a car

– Buying a house

Most people are borrowing to purchase:

– Cars

– Homes

But these do not generate any profit, unlike investment loans.

If you borrowed 10 million yen for an investment, there’s a chance for returns.

But with cars and homes, that’s not the case.

A private residence or a car doesn’t generate income—

so it’s considered bad debt.

This is something people really need to think about carefully.

Conclusion:

Financially elite households are typically debt-free,

while around 20% to 40% of the general population is living with debt.

Special Thanks OpenAI and Perplexity AI, Inc