管理人オススメコンテンツはこちら

「193万円の節税になります|知らなきゃ損!iDeCoの真実と落とし穴」

〜前回のつづき〜

●本当に効果のある節税方法ランキング解説(つづき)

第4位 『iDeCo』ですね。

(オススメ度★★★☆☆)

これは

名前を聞いた事が

有るかもしれません。

individual-type Defined Contribution pension plan

の略称です。

老後資金を貯めるための

お得な制度です。

投資信託(ファンド)に投資して

資産運用出来る。

投資信託やファンドというのは

『投資商品の詰め合わせパック』

だと思ってもらえればよろしいかと思います。

企業年金が無い会社員の場合

最大で月に23,000円の積立が

可能になってくるんですね。

iDeCoには

2つの大きな節税メリットが

有るんですね。

メリット(1)掛金が所得控除になる

掛金×所得節税分の税金が安くなる。

それから資産運用で儲けた利益が

非課税なんですね。

これも

よくわからないというのであれば

今日はiDeCoメインで

お話ししている訳ではないので

参考程度に読んで下さい。

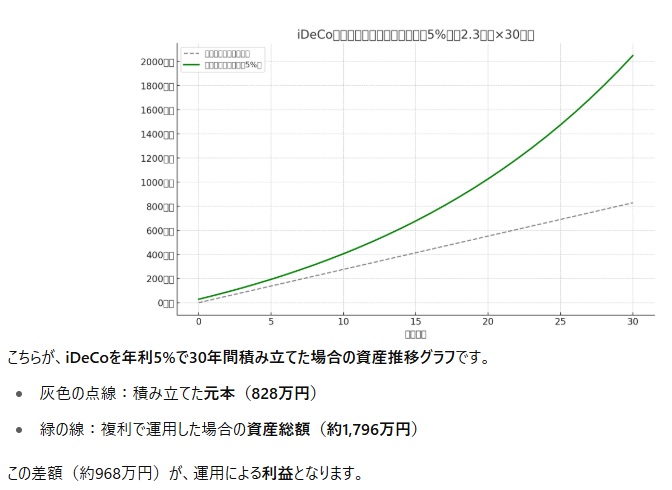

事例を見てみましょう。

30歳でiDeCoに加入して

月に2万3千円を12ヶ月×30年

60歳までずっと

毎月積み立てて

総額約828万円を

運用したとしましょう。

仮に年利5%で運用出来た場合

60歳時点で総額828万円貯めてたものは

1,796万円まで増えてるんですね。

運用益968万円に対する20%が

非課税なので

193万円の節税になります。

掛金の所得控除の節税効果を無視しても

これだけの節税になるという事になります。

注意すべきはこのiDeCoの場合

資金拘束が

強くて長いんですね。

60歳以降になるまでは

途中で必要であっても

引き出せないんですね。

ここがiDeCoのデメリットです。

運用に失敗して

マイナスになってしまうと

節税でも何でもなくなってしまう。

運用して上がった利益に対して

税金がかからないという事になるので

運用に失敗してしまうと

節税でも何でもなくなってしまう

という事です。

あとややこしいのが

掛金は控除になるんですけど

60歳以降に受け取る時に

結局税金がかかるんですよ。

利益に対しては

税金はかからないんだけど

受け取る時に結局税金が掛かるという

非常にややこしい話なんですけどね。

どれぐらい税金がかかるのかというと

・一括

・年金

の受け取り方によって

変わってくるんですね。

だからまだまだ

使い勝手が悪いんですね。

そういう所で

オススメ度★★★☆☆という評価です。

第4位とさせてもらいました。

〜〜〜つづく〜〜〜

Special Thanks college president Ryo.

●おまけ

≪≪Chat-GPTくんによる要約→perplexityちゃんによる文章まとめ≫≫

iDeCo(個人型確定拠出年金)は、老後資金を効率よく貯めるための制度です。毎月の掛金が全額所得控除となり、所得税や住民税が軽減される上、運用益も非課税になるという大きな節税メリットがあります。

例えば、月2万3千円を30年間積み立て、年利5%で運用できた場合、約830万円が約1,800万円まで増え、運用益にかかる約200万円分の税金が非課税となります。ただし、60歳まで原則引き出せない資金拘束の強さや、運用次第で元本割れするリスク、受け取り時に課税される点など注意も必要です。

長期的な資産形成には有効ですが、使い勝手やリスクを理解した上で活用しましょう。おすすめ度は★★★☆☆です。

Citations:

[1] https://money-bu-jpx.com/news/article058448/

[2] https://life.oricon.co.jp/rank_certificate/special/ideco/amendment/

[3] https://aoi-mirai.jp/blog/2025/02/89627/

[4] https://bizarq.group/column2/109/

[5] https://media.monex.co.jp/articles/-/26456

[6] https://dc.rakuten-sec.co.jp/lp/entry_rightnow03/

[7] https://news.yahoo.co.jp/articles/a074f978ce77dc1d247bdb32f9cc1d55baabb160

[8] https://i-exceed.co.jp/2025/04/03/2025年度税制改正:idecoの新たな可能性と注意点/

[9] https://www.ideco-koushiki.jp/simulation/

[10] https://www.freee.co.jp/kb/kb-trend/ideco-amendment-2024/

≪≪Chat-GPTくんによる英訳≫≫

~Continuation from the Previous Discussion~

【Explanation of the Most Effective Tax-Saving Methods (Continued)】

4th Place: iDeCo

(Recommendation Rating: ★★★☆☆)

You might have heard the name before.

It’s a beneficial system designed to help you save for retirement.

It allows you to invest in mutual funds and manage your assets.

Think of mutual funds as a “bundle pack” of investment products — that’s the easiest way to understand them.

For employees who don’t have a corporate pension plan,

you can contribute up to ¥23,000 per month.

There are two major tax-saving benefits to iDeCo:

Benefit (1): Contributions are income tax deductible

Your taxable income is reduced by the amount of your contributions.

Benefit (2): Investment profits are tax-exempt

If you’re not quite sure what that means,

don’t worry — since today’s focus isn’t solely on iDeCo,

you can just take this as general reference.

Let’s look at an example.

Suppose you start contributing to iDeCo at age 30,

putting in ¥23,000 per month for 12 months × 30 years.

That means you’ve consistently saved

until age 60, totaling about ¥8.28 million.

Assuming an annual return of 5%,

that amount could grow to ¥17.96 million by the time you’re 60.

The profit is ¥9.68 million.

Normally, 20% tax would apply to that,

but under iDeCo, it’s tax-exempt — saving you about ¥1.93 million in taxes.

And that’s just from the tax-free investment gains —

not even considering the tax savings from income deductions.

However, one thing to be aware of is the strong and long-term lock-in of funds with iDeCo.

You cannot withdraw your money until you turn 60,

even if you urgently need it.

That’s one of iDeCo’s major drawbacks.

If your investments perform poorly and result in a loss,

there’s no tax benefit — the whole point of the tax-saving mechanism disappears.

Since the gains are only tax-free when you make a profit,

losses mean no benefit at all.

Another complicated point is that,

although your contributions are tax-deductible,

you are taxed when you withdraw the money after age 60.

While investment gains aren’t taxed,

the money you receive is, which makes things a bit confusing.

The amount of tax you pay depends on how you withdraw:

As a lump sum

As regular pension payments

So overall, the system is still somewhat inconvenient to use.

Because of these factors,

it gets a ★★★☆☆ recommendation rating.

That’s why iDeCo ranks 4th.

Special Thanks OpenAI and Perplexity AI, Inc